Will Fiscal Austerity Work Now?

An update on some developments on the fiscal-trap front: After a Levy brief on fiscal traps was issued in November, events continue to bear out the fears expressed therein that budget cuts and tax increases being implemented in Europe and the US would lead to disaster. For example, recent news coverage of events surrounding the announcement of the UK budget confirm that the trap can hit nations that possess their own currencies, particularly in a region such as Europe where recessionary forces are dominating at the moment. Martin Wolf notes that owing to disappointing growth figures, the UK deficit surprised again on the high side. As the fiscal-trap theory asserts, governments implementing austerity policies have run into unexpectedly low growth in their attempts to reduce government debt.

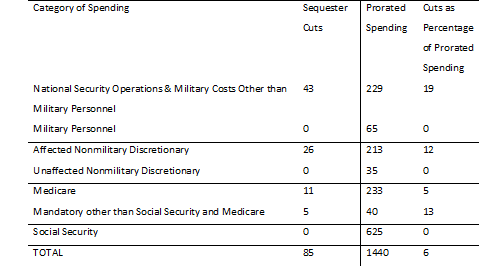

Meanwhile, despite the warnings of macroeconomists, including those here, the austerity measures that together make up the fiscal cliff in the US were only partly averted. Among these policy changes are the loss of the 2-percent partial payroll-tax holiday and the sequester cuts to discretionary spending. The latter unfortunately went into effect at the beginning of this month, following a two-month Congressional reprieve. Based on unofficial data from the Bipartisan Policy Council in this New York Times article, which are similar to those in a recent and more detailed CBPP report, the cuts for the remainder of the fiscal year are large as a percentage of planned spending, as seen in Table 1:

Dollar amounts shown in billions.

The bare mathematical essence of the austerity trap is summarized well in this blog post by Paul Krugman. In a trap, spending cuts and tax increases are self-defeating.

Speaking broadly, in order to measure the deficit in terms of the country’s wherewithal to pay taxes, one can look at it as a percentage of total GDP, as in the following formula:

(spending — tax revenues + debt service payments) divided by GDP

Keynesian economics shows that spending cuts and tax increases tend to reduce economic growth through their effects on aggregate demand. Hence, as Krugman points out, these policy changes tend to increase the quantity above for two reasons:

1) lower growth implies a lower denominator; and

2) lower growth reduces tax revenues

In the longer run, cuts in government spending on infrastructure, education, etc., also may reduce the productivity of workers, equipment, etc., and these supply-related effects further undermine GDP growth. The bottom line is that deliberate deficit-cutting policies implemented during periods of weak or negative growth tend to be futile, frequently increasing deficits as a percentage of GDP.

(Some caveats: Of course, our analysis of the possibility of a trap is about overall spending and taxation policies, not about particular government programs or taxes, which may or may not be growth-enhancing over the long run. Our discussion here is meant to focus on the topic of the brief: broad fiscal-policy trends around the world.)

Amidst the signs of fiscally induced problems around the world, keep in mind Hyman Minsky’s argument that economic instability mostly originates in the private sector. Indeed, financial crises involving real estate and the recessions that ensued are the main reasons that government deficits ballooned late in the last decade in many countries. In other words, fiscal traps do cause havoc, but the misguided fiscal policies in question were implemented mostly in reaction to crises that were well underway.

I hope to post more in the coming months on macroeconomics in theory and practice.

For a shortened version of the brief, see this synopsis in EUROPP, a European policy and politics blog.

ShareThis

ShareThis