Germany’s Über-Economists Are Rampant Again

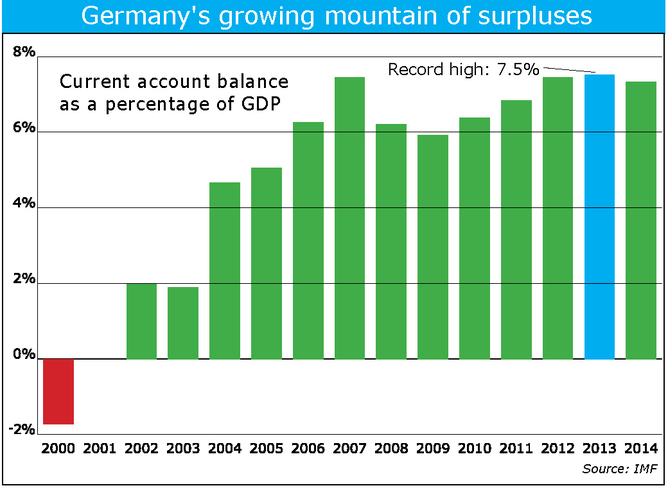

The rest of the world is holding its breath as the eurozone continues wobbling along the brink of deflation. In fact, numerous member states are already experiencing what it means to let “it” happen again. With the region stuck in depression since 2008, Euroland authorities are writing fresh world records in failing to improve the well-being of their citizens. The only thing that keeps rising in the eurozone is indebtedness—as the unsurprising consequence and symptom of its collective austerity insanity.

But that is not how the German authorities, or for that matter German economists, view the world. Blatantly ignoring the dismal facts that their favored medicine has produced, they never tire of calling for more of the same: austerity, austerity, and another extra dose of austerity please. By contrast, anything that might possibly help to turn fortunes around gets rejected out of hand as conflicting with the requirements of stability-oriented policymaking. In Germany, neither facts nor economic theory matter at all, it seems. Policy prescriptions simply have to match the ruling austerity-cum-competitiveness ideology, no matter what.

Hans-Werner Sinn, president of Munich’s IFO think tank, provided us with a fresh sample of German economic wisdom about a month ago, calling on Germany’s Chancellor Angela Merkel to stop ECB President Mario Draghi from even trying to regain control over its primary price stability mandate, defined as “below but close to two percent” inflation. Eurozone HICP inflation is currently running at only 0.3 percent. But even the thought of the ECB purchasing government bonds is giving rise to hyperinflation fears among German economists, it seems. It’s all a matter of principle and firm belief.

Professor Sinn is known to readers of Germany’s tabloid Bild-Zeitung as the country’s smartest economist. As if to confirm this popular verdict, Professor Sinn was at least making one valid point in his FT op-ed: namely, that the ECB has finally stopped ignoring super-low inflation while the eurozone’s political leadership remains stuck in denial. As the political authorities continue dreaming their austerity-boosts-growth delusion, the ECB (at last) has started devising actions intended to stop the nightmare reality from getting worse. To be sure, it is not an enviable position for any central bank to be in. The ECB is learning the hard way that not having a euro treasury partner means doing the tango on your own (which may look somewhat curious, if not ridiculous). But perhaps some central bankers have come to realize that not even trying to solo-dance might be judged as gross negligence should the eurozone end up sinking into full-blown deflation and chaos.

Professor Sinn reminds his fellow German citizens that they may petition the German Federal Constitutional Court in case they fear that their country’s Basic Law gets trampled upon. The law says that Germany can transfer monetary policy to a European institution that is independent and committed to the primary goal of price stability. This would seem to open up the interesting possibility that the court, if petitioned by its citizens, could also force German politicians to take action against the Bundesbank for failure, as part of the Eurosystem, to effectively stem deflation. Of course this is not exactly what Professor Sinn has in mind. It is utterly inconceivable that Germans, supposedly scared of nothing else in the world but hyperinflation, could ever worry too much about the opposite threat wreaking havoc across Europe—even as destructively-low inflation has been the reality for quite some time now.

And then there is Otmar Issing, formerly a professor of economics at Würzburg University and chief economist at the Bundesbank and then the European Central Bank. His recent FT op-ed is a response to worldwide calls on Germany to change its steadfastly-held austere fiscal stance and finally help the eurozone to recover. Here is Professor Issing’s diagnosis of the situation: continue reading…

ShareThis

ShareThis