Otmar Issing can look back on a long and consequential central banking career. Even in his retirement he is still living the part, evaluating whether his successors at the European Central Bank are pursuing stability-oriented monetary policies to his liking. His most recent critique (“‘Living in a fantasy’: euro’s founding father rebukes ECB over inflation response” https://www.ft.com/content/145b6795-2d21-48c6-984b-4b05d121ba16) shows him on the wrong side of events and debates about sound monetary policy, again.

Mr. Issing spent an eight-year stint at the Bundesbank as chief economist of Germany’s legendary central bank and retired guardian of European monetary affairs. Misled by M3 overshots that were the result of the Buba’s own rate hikes inverting the yield curve, Buba kept on hiking until it crashed newly unified Germany, and the ERM too. Recession-caused fiscal troubles then saw Mr. Issing’s Buba cheerleading pressures for fiscal austerity. These involved hikes in indirect taxes and administered prices that were distorting headline inflation upwards and delaying Buba easing (see https://www.levyinstitute.org/publications/on-the-burdenr-of-german-unification). The ensuing malaise in Europe was so pronounced that it almost prevented Mr. Issing from becoming a founding father of the euro.

But the euro got lucky, courtesy of a last-minute push from America’s dot-com boom. And so Mr. Issing got his chance as the ECB’s influential first chief economist. Unfortunately, lessons from Germany’s debacle ten years earlier were not learned. continue reading…

Lekha Chakraborty

(Professor, NIPFP, and Member of Governing Board, International Institute of Public Finance, Munich)

Climate change is about risks and uncertainty. How well the monetary policy stance can incorporate such risks and uncertainties is questioned by many economists. There is a broad consensus among economists that fiscal policy is capable of dealing with the climate crisis but monetary policy is not, due to the latter’s lack of tools. It is widely acknowledged that public finance commitments are essential to lowering carbon emissions. Public finance interventions—through taxation to reduce carbon prints or through public expenditure to support green energy and technology—have proven to be effective in reducing emissions. However, such empirical evidence is absent in the case of monetary policy.

India was the first to integrate a climate change criterion in its inter-governmental fiscal transfers. The macroeconomic policy channel of these “ecological fiscal transfers” works through the prioritization of public expenditure on climate change commitments by subnational governments, to make a “just transition” towards a sustainable climate-resilient economy. continue reading…

As the Reserve Bank of India Governor Shri Shaktikanta Das puts it upfront, these are extraordinary times, and we need to respond with “whatever it takes” to deal with the pandemic. Over the past few days, our hope for systematically “flattening the curve” by containing the COVID-19 pandemic and moving to a quick V-shaped or U-shaped recovery is waning[i]. Evidence is increasingly pointing towards the situation worsening to a dual crisis — a public health crisis and a macroeconomic crisis — like never before.

The IMF projections substantiate that the drag of the pandemic on global growth could be to the extent of -3%. This is a major revision in the global growth rate over a very short period of time. The IMF highlighted that “the Great Lockdown is the worst economic disruption since Great Depression, and far worse than the global financial crisis,” and its estimates suggest that “the cumulative loss to global GDP over 2020 and 2021 from the effects of the COVID19 pandemic would be around $9 trillion, greater than the economies of Japan and Germany combined.”[ii] *(The IMF has since released its latest [June 2020] estimates, showing global growth declining 4.9 percent, for a cumulative, 2020-21 loss of $12 trillion.)

How have the central banks responded to this crisis? This is evidently uncharted territory for the central banks — how to deal with “life versus livelihood” issues. The pandemic economics of central banks is twofold. One is the focus on measures that relate to instantaneous economic “firefighting”: for instance, how to ensure liquidity infusion into the system to stabilize the market reactions. The second is the long-term policy imperatives. As this crisis is of an unprecedented scale, it calls for unprecedented policy responses. continue reading…

The global market was eagerly waiting for the July Monetary Policy Statement of the Bank of England (BoE). Speculation was rife that, post Brexit, the BoE would become the latest entrant into the set of central banks experimenting with negative interest rate policy (NIRP) in a desperate bid to reinvigorate its economy.

Remember that the global financial markets were shaken after the referendum result and the pound plunged to a three-decade low. The BoE governor Mark Carney had to step in with a pledge to provide $345 billion for the financial system of the country. He also issued a statement that “the BoE has put in place extensive contingency plans” to deal with a “period of uncertainty and adjustment.” Analysts had their own predictions regarding the BoE’s possible monetary policy stance. JPMorgan Chase & Co., Goldman Sachs, and ING Bank were of the opinion that the BoE could lower its key interest rate in its July meeting. The result of a Bloomberg survey showed that in the event of Brexit, credit-easing measures such as quantitative easing (QE) and rate cuts may be the immediate options resorted to. The global importance of Brexit could be gauged from the fact that the Fed has had to delay to the fourth quarter of this year its plan of a possible interest rate hike in a bid to support global economic recovery.

However, the market was left surprised by the BoE’s decision to maintain its bank rate unchanged. The Monetary Policy Committee at BoE voted 8-1 to leave borrowing costs at 0.5 percent and hinted that it would launch a stimulus package in August. Today, the BoE reduced rates to 0.25 percent.

But why did NIRP not find favor with the BoE? After all, by the end of March 2016 as many as six central banks had adopted NIRP in an attempt to counter sluggish growth and deflationary pressures (fig 1). The latest country to join this mad race is the Bank of Japan, which announced in its January 2016 monetary policy statement a negative interest rate of –0.1 percent to current accounts that financial institutions hold at the Bank. continue reading…

Writing in The Hill, Paul McCulley argues that his profession’s fussy obsession with the Fed’s zero-point-whatever monetary policy is leading us into a dead end: “after a financial crisis, itself spawned by bursting of a bubble in private-sector debt creation, the power of monetary policy to generate robust aggregate spending growth is severely truncated.”

The policy problem we need desperately to solve — whose solution is key to a robust recovery, McCulley argues — is fiscal: “fiscal deficits need to be dramatically bigger.” To that end, he adds, it’s time to place the concept of “central bank independence” in its proper context:

Central bank independence has its time and place. But when economic growth is milquetoast and the reality is that inflation is too low, not too high (with the risk of outright deflation in the event of a recessionary shock), there is no reason whatsoever for the monetary and fiscal authorities to act independently — as if they were oil and water — in pursuit of the common public good.

Right now, what the country needs is for the fiscal authority to exercise its latitude to purposely ramp up its spending more than its taxing, and for the monetary authority to print however much money is necessary to keep interest rates low, unless and until inflation smacks the economy in the face. And the fiscal and monetary authorities need to openly declare that these actions are a political joint venture.

Yes, my profession needs to remember that macroeconomics, as a discipline, is about solving collective action problems. The solutions are often politically messy, offending the sensibilities of the moneyed class. Such is the nature of effective democracy: Messiness that delivers for all.

Confusions about so-called helicopter money (HM) continue unabated. My recent letter to the editor of The Financial Times, titled “’Helicopter money’ is a muddled fiscal policy by another name,” has not met with universal approval. In fact, it seems to have ruffled some feathers and caused some annoyance.

Simon Wren-Lewis is a case in point. In a response to my letter (and a piece in the FT by John Kay) published on the Mainly Macro blog, Wren-Lewis reiterates his concerns that trying to distinguish fiscal from monetary policies is ultimately pointless and that central banks need to have HM in their armory since otherwise delegating stabilization would be dangerously incomplete. Mr. Wren-Lewis is perhaps best known for his selfless efforts at trying to wring any sense out of mainstream macroeconomics – an endeavor that takes a lot of wringing indeed. Another case in point is fellow helicopter warrior J. Bradford DeLong, who re-published Wren-Lewis’s HM elaborations on his own blog with the remark “intellectual garbage collection.” The wisdom of HM is just too obvious to be challenged, it seems.

But first recall here that Bradford DeLong is the supposedly “New Keynesian” macroeconomist who a few years back published a piece titled “The Triumph of Monetarism?” in the Journal of Economic Perspectives, arguing – quite correctly actually! – that New Keynesianism was really muddled New Monetarism by another name. It is also the same new monetarist economist who not so long ago published a piece together with Larry Summers titled “Fiscal Policy in a Depressed Economy,” in which the two argued that the time was right for governments to ramp up their investment spending and not worry about debt. That argument made quite a bit of sense to me at the time – and it still does today, as I suggested in my FT letter.

In any case, I was quite amused when at an event at the Brookings Institution on May 23 Larry Summers proclaimed that: “Helicopter money, hear me, helicopter money is fiscal policy. There is no such thing as helicopter money that isn’t fiscal policy.” That may well be just yet another useless point to make of course. But I will leave it to Messrs. Wren-Lewis and DeLong to do the intellectual garbage sorting of Mr. Summers’ remark.

Moving on, a rather interesting piece was published on VoxEU by Claudio Borio (together with Piti Disyatat and Anna Zabei). Borio’s earlier research at the BIS focused on central banks’ operating procedures. He isn’t someone who can be easily fooled about what central banks are doing or not doing. Furthermore, and this may not be a coincidence, he is also one of those rare cases among monetary economists who clearly identified what I long ago dubbed the “loanable funds fallacy” in Ben Bernanke’s “saving glut hypothesis” (see here). continue reading…

In the Financial Times, Jörg Bibow writes in reaction to an article by Stephanie Flanders on “helicopter money” — the idea of having the central bank directly credit citizens’ bank accounts (or, in the thought experiment, to print bank notes and drop them from helicopters) with the aim of generating increases in consumer spending.

Bibow observes that helicopter money is really just fiscal policy, properly understood, and adds that it is preferable that elected fiscal authorities actually do their job — increase spending — during a period of inadequate demand; perhaps by investing in the “energy infrastructure,” as Bibow suggests.

The Federal Court of Accounts (TCU) announced in 2015 that it had rejected the accounts of Rousseff’s administration for the year 2014. In a unanimous vote, the TCU ruled Dilma Rousseff’s government manipulated its accounts in 2014 to “disguise fiscal deficits” as she campaigned for re-election. The allegation is that Ms. Rousseff manipulated Brazil’s account books to hide a growing fiscal deficit.

The argument is that the federal government borrowed money from public banks (which is forbidden by the Fiscal Responsibility Law) to pay for social programs. So, they argued she allegedly committed an administrative crime.

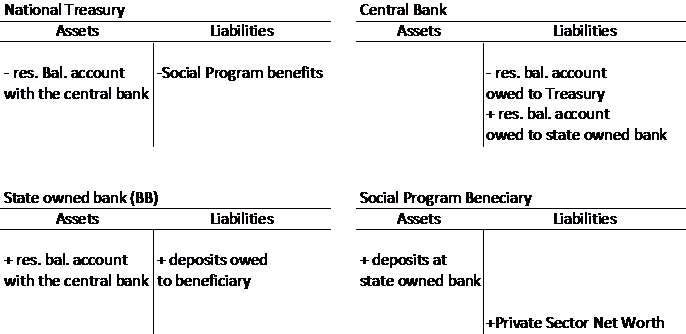

Once we understand how the government spends and what bonds are for, then we can analyze TCU’s decision. The Treasury has an account—known as Treasury Single Account—with the central bank. When the Treasury spends, its account with the central bank is debited and the bank’s account with the central bank is credited. This is followed by a credit to the beneficiary’s bank account. That is, the public bank then makes payments to the social program beneficiary by issuing deposits (Case 1).

Case 1. The Treasury spends using its account with the central bank

The issue at hand is that the federal government made payments for social programs using its public banks but it delayed payment to the same banks. That is, the federal government did not use its account at the central bank to credit the public banks’ account with the central bank while public banks made those social benefits payments. So, public banks made the payment (by creating demand deposits) and on the asset side there was an increase in credits (“loans”) to the Treasury (Case 2), which is forbidden by the fiscal responsibility law. In a “normal” transaction banks’ reserve balances (that is, government IOUs) with the central bank would go up, but because the Treasury delayed payments to banks there was in increase in balances owed by the Treasury to the public banks. This led the TCU to conclude that this was a “financing” operation. continue reading…

ShareThis

ShareThis