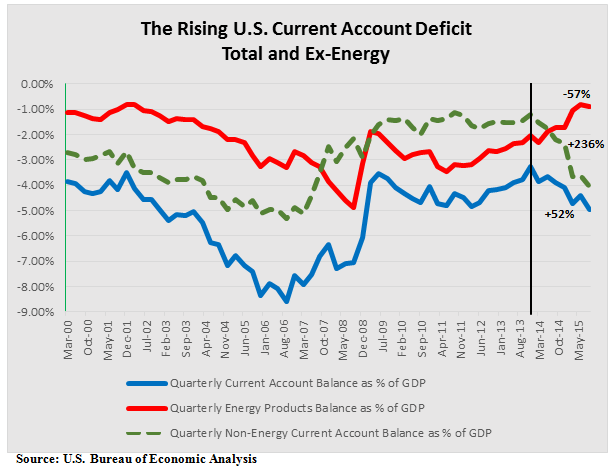

Stormy Fantasies about Labor Cost Competitiveness

Lamenting that intellectual inertia is responsible for slow progress in economics, Servaas Storm sets out to teach a lesson to everyone who may still be foolish enough to believe that relative labor costs matter for international competitiveness and that diverging unit labor cost trends – specifically persistent wage moderation in Europe’s largest economy, Germany – may have played a rather critical role in sinking Europe’s monetary union. It is a dangerous myth, Storm proclaims, that labor costs drive competitiveness. He suggests that the eurozone crisis originated from a different set of causes altogether; German wages are little more than trivia.

I fear that Servaas Storm will further add to existing confusions about both German wages and the widely misdiagnosed and never-ending eurozone crisis more generally. His blog of January 8, 2016 titled “German wage moderation and the eurozone crisis: a critical analysis” (see here) is hardly a masterpiece in analytical coherence. I will focus on some key issues.

Storm appears to be making three big points. First, German wage moderation is a mere fiction. If Germany’s competitiveness improved at all under the euro, that was the result of nothing else but its engineering ingenuity: “It was German engineering ingenuity, not nominal wage restraint or the Hartz ‘reforms’, which reduced its unit labor costs. Any talk of Germany deliberately undercutting its Eurozone neighbors is therefore beside the point.” Second, Storm essentially agrees with the “consensus narrative” recently proposed by a group of CEPR-associated researchers (see here) which sees the origin of the eurozone crisis in rampant capital flows causing massive intra-eurozone current account imbalances. German wage moderation does not feature at all in the consensus narrative, a conspicuous neglect that prompted Peter Bofinger’s recent critical response (see here; and also here). Storm’s attack therefore reserves some special venom for Bofinger (amongst various other proponents of the wage moderation hypothesis, including this author). Third, the eurozone’s real underlying problem, according to Storm, is that the euro has “not led to a convergence of member countries’ production, employment, and trade structures, but rather to a centrifugal process of structural divergence in production.” Somehow – but other than through wage moderation! – Germany got even stronger in high value-added, higher-tech manufacturing under the euro, while the eurozone South remained stuck with low value-added, lower-tech manufacturing.

In the course of presenting these three points (or hypotheses) Storm not only thoroughly misrepresents the “wage moderation hypothesis,” he also fails to shed any new light on the supposed role of capital flows, while ending up with the rather disheartening proposition that the euro is essentially nonviable until the eurozone’s production structures converge to the German standard.

Regarding the first point, the idea that German wage moderation may be fiction rather than fact, I am simply baffled. The wage moderation hypothesis (at least as I have presented it; see here, here, and here, for instance), starts from the following facts (data courtesy of Eurostat and the OECD). First, Germany’s unit labor cost trend stayed persistently below the common stability norm as set by the ECB; reneging on the golden rule of currency union. Second, German wage inflation was the clear outlier in the downward direction. Third, German productivity growth barely met the euro area average. continue reading…

ShareThis

ShareThis