The Only Graph Needed to Explain the New Year’s Dive of 2016: Larry Summers Sort-Of Gets It, the Fed Doesn’t Seem to Get It, and the Media Seems Hardly Aware of It

by Daniel Alpert

A practically unnoticed phenomenon underpins the negative U.S. economic data trends we saw in Q4 2015 and the enormous increase in market volatility in the first week of 2016: the United States’ global competitors are—once again—using vast pools of low-wage, underutilized labor, a huge excess of domestic production capacity, and/or the ever-stronger U.S. dollar, to grab whatever share of demand they can in order to maintain/recover growth in a sluggish global economy.

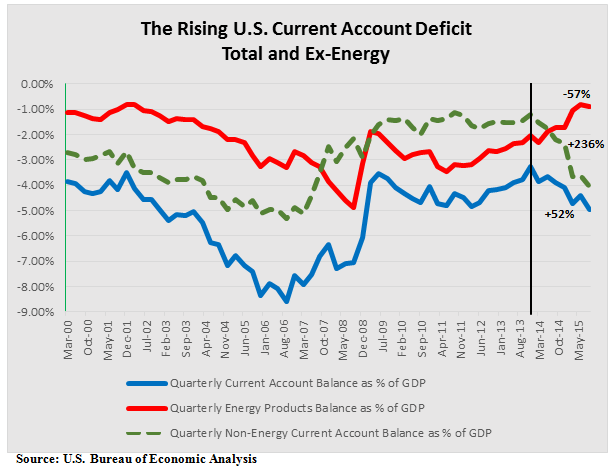

While the plummeting price of energy—the result of insufficient global demand and huge new oversupply from North America itself—has cut America’s energy deficit to a level less than 20 percent of its 2008 peak, the overall current account deficit of the U.S. grew rapidly in 2014 and, more alarmingly, in 2015. The nation’s current account is the sum of the balance of trade (goods and services exports less imports), net income from abroad and net current transfers.

But here’s the brutal bottom-line: the non-energy portion of the U.S. current account deficit, relative to GDP, has ballooned by 236 percent since its low in December 2013, during which period the energy deficit fell by 57 percent.

The U.S. economy is showing weakness in Nearly Everything But Employment (“NEBE”) and even its salutary pace of job formation is plagued by an unusual level of temporary and low wage hiring, painfully low labor force participation and very low levels of nominal wage growth. Consumption is therefore not rising in a manner anywhere near the rise in headline job formation. And the demand-push inflation that one would normally expect to have emerged with the creation of 5.6 million jobs over 24 months is nowhere to be found. In fact, the U.S. is joining the rest of the world in a persistent pattern of alternating deflation and disinflation (“lowflation”).

The substantial slowdown in China, the evident failure of Abenomics in Japan, the collapse of the Brazilian and Argentinian economies, and a failure of the eurozone to get off the mat despite the “anything it takes” monetary posture of the European Central Bank, have all contributed to declining global aggregate demand for all sorts of production. This has been reflected particularly acutely in the energy and other commodities sectors.

All of the foregoing constitute a bitter pill for the United States economy which, better than any other, was able to substantially reduce its trade deficit from the end of the recession through 2013 and to lever its size, its willingness to engage in extraordinary monetary easing early and often during and following the Great Recession, and its inherent resiliency to produce at least a tepid recovery while other regions slowed or remained mired in slump.

After all its deft maneuvering, the U.S. is once again being inundated by cheap imports and seeing its ability to export severely impaired, because of a combination of its competitors’ internal deflation and efforts (direct and indirect) to devalue their currencies relative to the U.S. dollar and each other’s. This is vastly constraining U.S. economic growth and may result in its contraction at some point during 2016.

This nearly universal beggar-thy-neighbor behavior has all the makings of a very serious global economic disruption and proceeds from the same global economic imbalances that we saw before, during and after the Great Recession; the vast oversupply of labor, production, and capital relative to aggregate demand for all three.

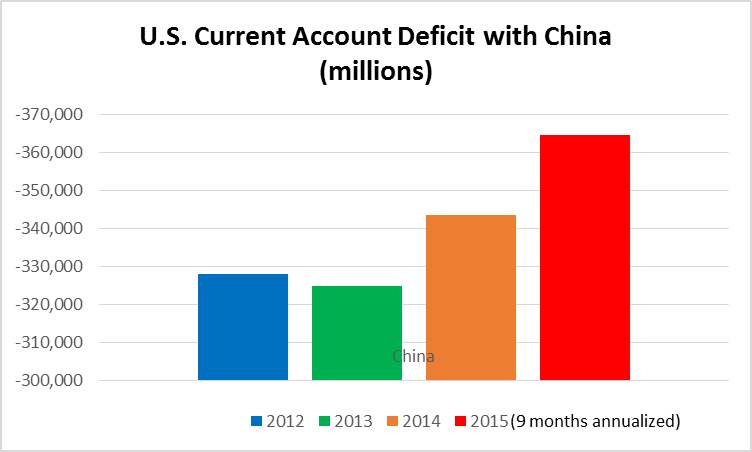

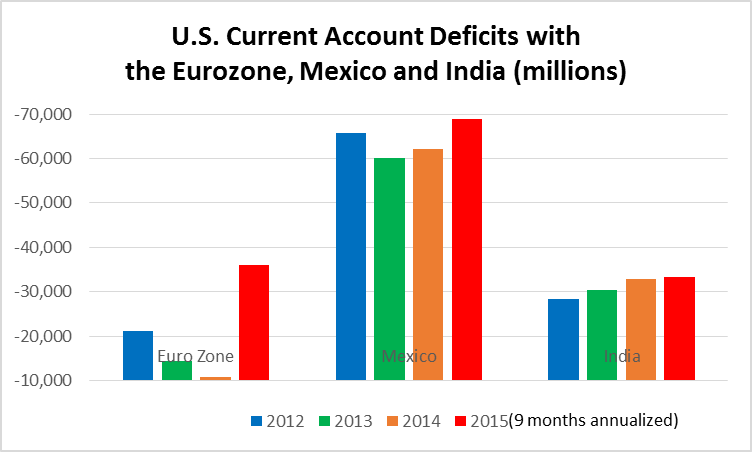

Where is this coming from? The below figures reflect the increased magnitude of current account surpluses of a handful of the U.S.’s trading partners:

Source: U.S. Bureau of Economic Analysis

Unfortunately, there appears to be a tendency among many of even the most concerned economists to avoid an emphasis on global economic imbalances when analyzing the U.S. economy. Larry Summers, who has been riffing Alvin Hansen’s secular stagnation meme since late 2013, has been most accurately describing the domestic phenomena that has the U.S. continuing its post-recession slump (or, more accurately, its slump in “NEBE”).

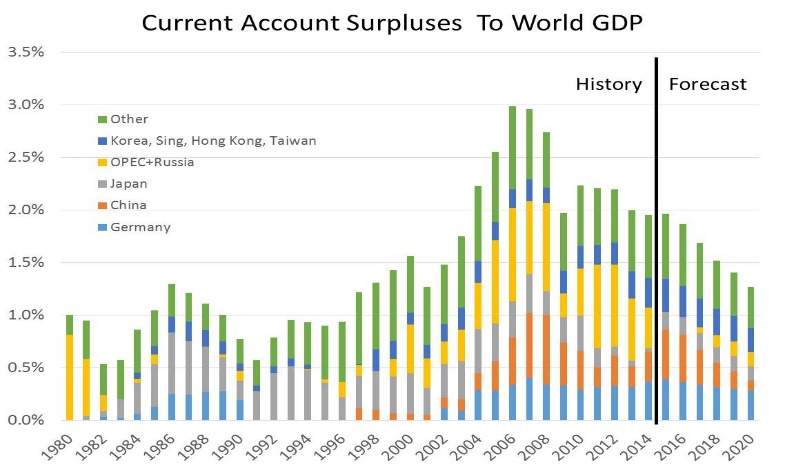

Summers certainly gets the insufficiency of demand issue, and correctly identifies the domestic causes of stagnation. In a November 2015 speech at the Central Bank of Chile, Summers noted that cross border surpluses and deficits are indeed relevant to what is transpiring, but he did so in the context of his friendly feud with former Fed chairman Ben Bernanke, who emphasizes their importance but views them as being transient. Indeed, Summers used the below figure in his talk to indicate (based on IMF data) his reckoning of why Bernanke may be right (in that the IMF believes global surpluses are likely to decline post-2015), while at the same time saying that the issue is a pressing one he is still thinking about.

Summers and Bernanke, and the IMF, are all missing the boat here, I feel. The imbalances that gave rise to huge current account surpluses on the part of the United States’ most competitive trading partners are not likely to decline any time soon. In fact, for the reasons stated above, I believe that they are going to grow again—as they have been. And, given these competitors’ motivations for and the ease of grabbing more than their fair share of global demand, I believe that we will shortly see the U.S. current account deficit, ex-energy, surpass even the elevated levels during the mid-2000s. And it is the ex-energy portion of the current account deficit that evidences the trade that really counts in terms of the economic health of the United States.

The Federal Reserve’s Open Markets Committee and staff appear to discount these imbalances almost entirely. With their excessive focus with job formation and headline unemployment rates (and corresponding de-emphasis of other aspects of the U.S. employment situation), the Fed takes current account imbalances and inflation and writes the whole disturbing business off as either unimportant or transient. Sadly, many of the Fed’s older economic models simply don’t weight global phenomena highly and newer thinking (even of Larry Summers’ variety, much less my own) is not weighted highly enough by FOMC members. Add to that the notion on the part of several members of the committee that the trade deficit merely reflects a classic healthy demand for non-energy imports, as the U.S. has fully morphed into a service economy (ignoring that much of that service economy involves the marketing and distribution of goods, and that as goods prices fall, so will the amounts firms will be willing to pay for such support functions), and you have something almost amounting to willful blindness to the issue.

As to the business and economic media, well, sorry to drop this on you so soon after the holidays, but here’s an angle that may prove to be the whole story in 2016. Get on it.

Daniel Alpert is Founding Managing Partner of Westwood Capital, a fellow in economics at The Century Foundation, and the author of “The Age of Oversupply: Overcoming the Greatest Challenge to the Global Economy.”

ShareThis

ShareThis