Euro Crisis Sees Reloading Of Germany’s Current Account Surplus

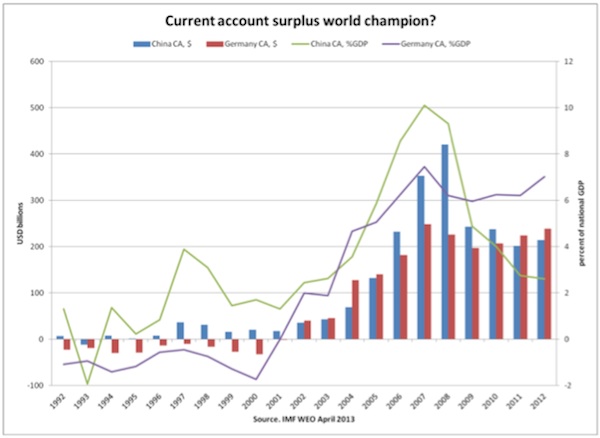

Who is running the largest current account surplus in the world? China? Saudi Arabia? Both wrong! These are only the number two and three countries. China had a record $420bn surplus in 2008, but that imbalance has more than halved since. As a share of GDP China’s external imbalance is down from ten to two-and-a-half percent since the global crisis — evidence of a remarkable rebalancing. The oil price would need to be significantly higher still to make Saudi Arabia the number one.

So for 2012 the number one prize actually goes to: Germany! The world champion of 2012 ran up a current account surplus of almost $240bn. At a rocking seven percent of GDP, that’s just slightly below Germany’s pre-crisis record of almost $250bn in U.S. dollar terms. In euro terms 2012 actually set a new record for Germany. And that is an interesting part of the whole story, as the euro has depreciated by some 20 percent from its peak against the U.S. dollar.

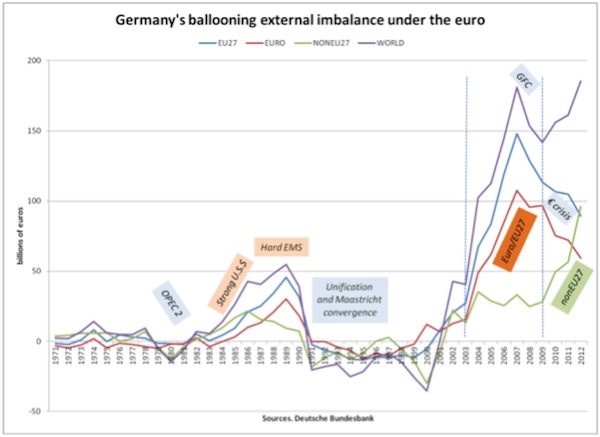

Back in the 2000s, the euro appreciated very strongly against the U.S. dollar (as well as in real effective terms) between 2002 and the summer of 2008. Euro appreciation cut Germany off from benefiting even more from the record global boom of the 2000s. However, somehow Germany, then also known as the “sick man of the euro,” managed to run up gigantic regional current account surpluses, both vis-à-vis its euro partners and vis-à-vis the larger European Union (of 27 member states). At its pre-global crisis peak Europe was the primary source of Germany’s current account surpluses. Don’t miss then what a remarkable re-loading and re-sourcing of German external surpluses has occurred since then.

Being so conspicuously export-dependent for its growth, Germany got badly hit by the global crisis of 2008-9. The German economy shrunk a whopping five percent in 2009. But Germany then enjoyed a stunning recovery in 2010-11. This partly owed to a surprising, very unGerman “Keynes moment” in German policymaking, a sizeable German fiscal stimulus. But it owed even more to the stimulus packages put in place by China and the U.S., which have recharged Germany’s export engine, and did so despite the ongoing Euroland crisis. So here is the remarkable re-loading and re-sourcing of Germany’s external surplus: surpluses vis-à-vis Euroland and the EU at large are sharply down, but the regional crunch was more than offset by surging extra-regional surpluses. So Germany got lucky once again, and no doubt this also owes to the weaker euro, conveniently depressed by the Euroland crisis.

Recall here that Germany’s main economic motivation for the euro was to prevent deutschmark strength from undermining Germany’s competitiveness within the region. Ballooning regional surpluses suggest that the euro paid off handsomely in this regard, it would seem. Today, by contrast, euro payoff takes the form of boosting Germany’s extra-regional competitiveness. Not so bad either, it would seem.

There is just one catch here. As one probably would not have guessed from the devastating and highly counterproductive policy prescriptions Germany has handed out to its crisis-stricken euro partners, Germany is actually highly vulnerable to crisis developments in Euroland. While still enjoying “haven status” as the markets remain anesthetized by Mr. Draghi’s big bluff, Germany has built up huge financial exposures to its euro partner countries – which are subject to loss, especially in case of euro breakup. In case of euro breakup Germany would also lose its global protection shield that is currently keeping the world champion in current account surplus production über-competitive, as a new deutschmark would likely be welcomed by an abrupt appreciation that would see the German economy crater as a result.

Germany’s vulnerability to the Euroland crisis is investigated in more detail in a new Levy Economics Institute working paper (no. 767) that has just been published here.

(this article first appeared in Social Europe)

ShareThis

ShareThis

[…] Quelle: Multiplier Effect […]

Dear Jörg Bibow,

I found your post very interesting and relevant. I have some comments to open a discussion.

Firstly, I want to underline that most of German external surpluses before the great financial crisis comes from European partners and from the United States. In contradiction with the story of an ultra-competitive Germany in emerging markets. In fact, Germany have a bilateral commercial deficit of about ten billions dollars with China in 2008.

Secondly, even if the share of European countries in Germany’s current account surpluses is declining. Its still represents about two thirds of its external surpluses. However, I agree with your the most dynamic part of the surpluses come from non-European countries as these countries have implemented large sending cuts.

Thirdly, you advocate that the depreciation of euro has played a major role in the persistence of current account surpluses after the crisis of 2008. The problem with this kind of analysis is that it neglects the fact that the most important determinants of price competitiveness is not the level of exchange rate but the distance the observed exchange rate and the equilibrium exchange rate.

We have now some evidences that Germany has benefited from an undervalued Euro from 2005. So between 2005 and 2008, the Euro has appreciated but this real effective appreciation was not too strong in regards of fundamentals of the German economy.

Yours sincerely

Jamel SAADAOUI

Associate Professor of Economics

University of Strasbourg