Beyond “Fixing” the “Fiscal Cliff”

The cliff approaches, and politicians and pundits in Washington are pondering how to deal with it. For those who have forgotten, recent nontechnical summaries of the legislative issues and amounts of money at stake can be found here , here, and in this old post. But essentially, the term “fiscal cliff” refers to a massive group of tax increases and spending cuts due to take effect on or around January 1 of next year. President Obama and some Congressional Democrats are seeking to take a stand for distributional fairness and deficit reduction at the same time by pushing for a renewal of the Bush tax cuts, but only for those with incomes less than perhaps $250,000 for a couple. On the other hand, some long-time fiscal conservatives are seeking to cushion the blow by delaying the impact of the spending cuts and tax increases and by seeking a less indiscriminate choice of program cuts. They emphasize that in any case, draconian measures must in their view be taken eventually and committed to now.

From the point of view of Keynesian macroeconomics, what the fiscal conservatives fail to understand is that the economy requires even more fiscal ease than they have been willing to contemplate so far; otherwise, like Spain and many other European nations (see the FT and the WSJ on the European austerity debate), this country will experience such weak economic performance that even the goal of reducing the deficit will be elusive—let alone feeding the hungry, keeping states and localities from going broke, maintaining an adequate defense, or funding scientific research.

The automatic spending cuts (known also as sequesters) due to take effect soon are designed to hit almost every discretionary defense and nondefense spending item—to the tune of 10- to 15-percent cuts in what the federal government spends each day on average on these items. The intent of the legislation that created the sequesters was to put in place a stick over the government’s head to force a big deficit reduction. Combining these sequesters with the other elements of the fiscal cliff (given the law as it stands now) gives us reduction in the deficit equivalent to about 4 percent of GDP early next year. Assuming a very modest multiplier of 1, the impact would be reduction in GDP growth of approximately 4 percent for 2013, leaving aside the offsetting effects of various automatic stabilizers that will still be in place. Of course, this is a very rough estimate, based on an imprecise rule of thumb. Estimated impacts of 6 or 8 percent would perhaps be equally reasonable, under the (unrealistic) assumption that Congress allows all of the spending cuts and tax increases to go into effect for the full calendar year.

The problem is that the government is trying to cut the deficit at a very bad time. Instead of seeking to return to a balanced budget, it needs to habitually increase the deficit whenever we are so far from full employment, perhaps with the help of a rule of some kind. As I pointed out recently, food stamps (like other means-tested transfer programs) help in this way, in addition to directing aid to individuals in need. A type of economics known as post-Keynesian Institutionalism (PKI) has emphasized such automatic stabilizers, which embed what amount to Keynesian “fiscal policy rules” in various permanent institutions. The adherents of PKI count Minsky and a number of other great economists as among their numbers. A 2011 book helps to define PKI and outline its views on macro policy in a nontechnical way: Financial Instability and Economic Security after the Great Recession, edited by Charles Whalen. (The publisher’s book website allows free access to the table of contents, preface, list of contributors, and more.) An article by David Zalewski and Whalen in this book touts automatic stabilizers in general and suggests a rule whereby states and localities would get additional funds from the federal government equal to a percentage of the year’s expected federal deficit, to help deal with low tax revenues during hard times. (By the way, Whalen is also the author of a recent Levy Institute working paper on PKI.)

Of course, another proposed “policy rule,” and indeed one strongly supported by Zalewski and Whalen, is a federal employer-of-last-resort (ELR) program. (I ought to mention that Pavlina Tcherneva, who is well known for her research on, and advocacy of, ELR programs, among other work, will be joining the Bard College faculty next year.)

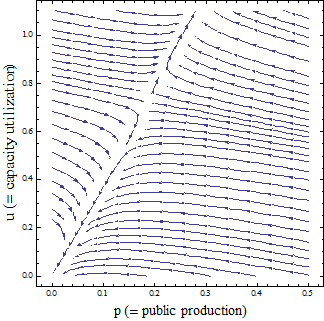

Recently, in my own research, I’ve been working on the effects of various kinds of fiscal policy in a post-Keynesian macro model. (Link to recent paper, which is somewhat technical. Link to earlier post on this model, with interactive graphics) Using simulations, I have found that a balanced-budget-targeting rule for government spending can lead to economic collapse (see figure below, which is from the paper), but an unemployment insurance program and a spending rule with dual public-production and capacity-utilization targets are policy rules that exert very beneficial stabilizing effects on the path that the economy follows over time.

As for the more immediate problem of the “fiscal cliff,” Robert Reich proposes a “trigger rule” whereby deficit reduction would be put off until the economy had reached goals of perhaps 3-percent-per-year GDP growth and an unemployment rate of less than 5 percent. Like many proposals now on the table, Reich’s idea would call for Congress to “repeal and replace” the impending sequester, etc., with more gradual deficit cuts. Especially in the case of the sequester, even repeal alone seems like a good idea.

ShareThis

ShareThis

It doesn’t enter my mind the “deficit” has to be a control variable instead of a resulting (dependent) variable. A major control variable should –to make economic sense in the promotion of public good–, be the desired level of employment of real resources that are available.

That is right; your comment seems a propos. On the other hand, there may be an issue of semantics that may be throwing me off a bit: I have used the word “policy target,” while you use the word “control variable,” but I gather that you are with me on the desirability of aiming for a specific capacity-utilization rate (or perhaps some similar target such as an employment rate), rather than a balanced budget, over the long or short runs. One reason is indeed that as an economic variable, the deficit is endogenous, or as you put it, “resulting” or “dependent.” Another is that there is no reason to regard a particular level of deficit spending as a social goal or end in itself; rather, as Abba Lerner argued, one should seek to meet the goals of full employment and low inflation and let the deficit adjust as necessary to achieve those ends. In other words, why would the prospect of perennial deficits matter, if we can anticipate good performance in terms of employment, inflation, etc., based on fairly long simulations of our proposed policies, and on historical experience with running deficits. (Of course, there are many other points to be made in support of Lerner’s position.) Thank you; I hope I have understood your comment.