Austerity and Growth: Missing the Point

The pseudo-debate about whether Keynesians and other fellow travellers ought to be embarrassed when governments that engage in fiscal austerity nevertheless experience positive economic growth rates has become a distraction.

For countries like the US and the UK, it is possible under current circumstances for governments to implement budget cuts and still see their economies grow. But the truth of that statement is not fatal to the Keynesian-inspired critique of austerity policies; it is not by any means the end of the story. The more meaningful question is this: What would have to happen in these economies for significant growth to occur in the midst of budget tightening?

Finding an answer to that last question is one of the strengths of the approach to thinking about the economy pioneered by Wynne Godley, and fleshed out further in the Levy Institute’s strategic analysis series. This approach also provides a clear understanding of how deeply irresponsible it is to cut government spending under present economic conditions: because the danger, given the state of the US and UK economies, is not just that budget cuts might slow down the economy, but that they might not.

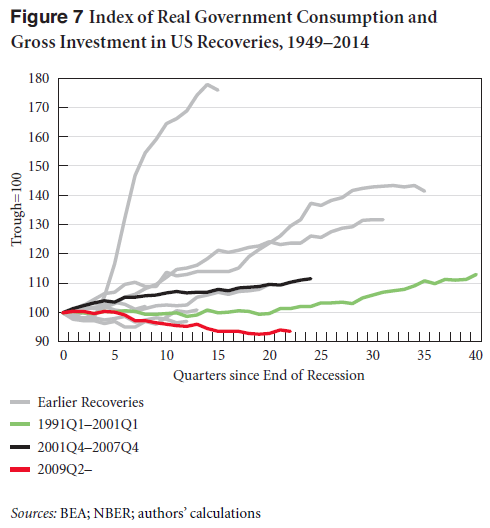

Let’s look at the United States in particular. In their just-released report, Dimitri Papadimitriou, Greg Hannsgen, Michalis Nikiforos, and Gennaro Zezza point out that, with the exception of a short cycle in the ’70s, “there has been no other recovery in the modern history of the US economy in which government spending decreased in real terms.”

The Congressional Budget Office is predicting that the budget deficit will continue to shrink over the next few years, from 2.8 percent of GDP in 2014 to 2.4 percent in 2018. At the same time, the authors note, the CBO is telling us that GDP will grow at 2.8 percent, 3 percent, 2.7 percent, and 2.1 percent in 2015, ’16, ’17, and ’18, respectively. If we assume that both of those forecasts (for the budget deficit and GDP growth) come true, what would the rest of the economy need to look like?

The United States has run current account deficits, which act as a drag on economic growth, for decades. And despite the recent increase in net exports of petroleum products, which has helped keep the US trade deficit from returning to its sky-high precrisis levels, there is little reason to think that the external deficit will substantially improve over the next few years (if anything, the authors argue, it is likely to get worse. There’s more on recent developments in the foreign sector beginning on p. 6 of the report).

That being the case, GDP growth rates of the sort projected by the CBO can only come to pass on the basis of a rise in private sector spending. In fact, Papadimitriou et al. show that private sector spending would have to expand so much that it would exceed private sector income for the first time since the crisis. In other words, growth would depend on rising private indebtedness.

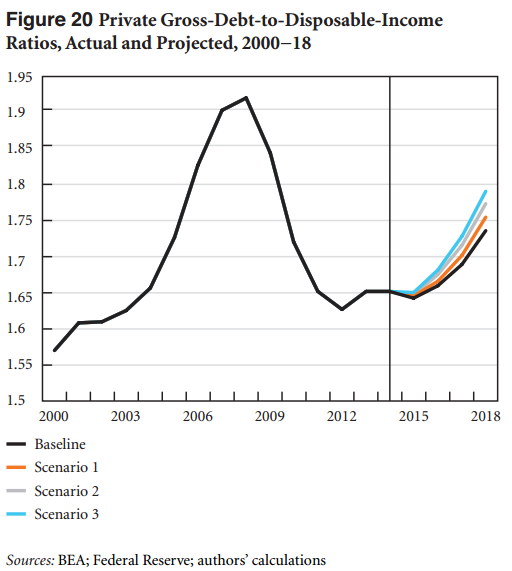

If the dollar continues to appreciate further and the economies of US trading partners end up performing worse than the IMF expects (a very real possibility, the authors point out, given the optimism of IMF forecasts), this increase in private sector spending over income — and thus the increase in the private debt-to-income ratio — would have to be even larger. Here’s what that would look like (in the chart below, “Scenario 1” corresponds to slower growth among US trading partners [by 1 percent of GDP annually], “Scenario 2” to a 25 percent appreciation of the dollar over the next four years, and “Scenario 3” to a combination of the two):

If private spending doesn’t blow up in this way, the CBO’s optimistic growth projections won’t come about. But if growth does occur, it can only do so (given the external deficit) through a process that raises the debt-to-income ratio of the private sector. As the authors point out, this is precisely the same process that led to the Great Recession and its aftermath.

What’s worse, the state of income inequality in the United States is such that this increase in private debt will be borne disproportionately by households in the bottom 90 percent of the income distribution. Unlike the federal government, which can service its debt through mere keystrokes, US households cannot sustain rising debt ratios of the sort portrayed in the chart above (though the amount of public hand-wringing spent on the debt of the former, as compared to the latter, would suggest the opposite). As Papadimitriou et al. write:

“Increased borrowing of one kind or another can often be sustained for a long time … but eventually, retrenchment takes place relative to incomes. The consequences of any further retrenchment in debt-financed consumer spending would be felt throughout industries that produce for the US consumer, and again, as we noted above, the recovery in real private domestic consumption is already weak relative to any previous recovery.”

To bring this back to the tired discussions surrounding austerity policies: yes, it is possible for the United States to have both tight budgets and rising GDP over the next few years. Fiscal conservatism doesn’t make economic growth impossible in the near term — it makes it impossible to grow without increasing financial fragility. In the absence of a significant increase in net exports, keeping the government budget on its current track will lead to either stagnation or an acute crisis.

Austerians in the United States and elsewhere have been allowed to portray themselves as the champions of steely-eyed realism and prudence. In reality, unless their budget proposals come attached with some workable plan to substantially reduce trade deficits, they are courting private-debt-driven financial crises. In any meaningful sense, they are the true practitioners of fiscal irresponsibility.

ShareThis

ShareThis

There is no direct relationship between private demand and private debt ratios. Households and businesses incur debt for many reasons other than expenditure on currently produced goods and services. The large majority of debt is incurred to finance changes in ownership of existing assets, not for spending that contributes to GDP. Over longer periods, changes in interest payments are also a major factor in the evolution of debt ratios, and again do not contribute to demand.

The denominator also matters. Faster growth and higher inflation reduce debt ratios, slower growth and lower inflation reduce them. Shifts in inflation have historically played a much larger role in changing debt ratios than have changes in current spending. With higher inflation — which is certainly possible — it is entirely possible for rising private demand to be associated with falling debt ratios.

Your claim that faster growth of private demand necessarily implies rising private debt ratios has no basis either in economic principle or in the historic record. You need to stop saying this.

Josh,

The issues you highlight are important. Obviously inflation and interest rates are important variables in the determination of the debt-to-income ratios and historically have played some role in the increase of the debt-to-income ratios of the private sector.

Note that we are not saying that faster growth in private demand necessarily implies higher debt ratios; we say it does given the current conditions (inflation, income inequality, etc).

The case you make is more convincing for the corporate sector ; where there is evidence that there has been a decoupling of investment decisions from cash flows (as you show in your recent paper). However, to produce our simulations we assume that the corporate sector will continue borrowing in the same way it has been doing since 2010, so it is not a change in the behavior of the firms that leads to reversal in the debt-to-income ratios of the private sector.

This reversal is related to the behavior of the households. When it comes to households—at least for the vast majority of them—there is convincing evidence that consumption expenditure is related to borrowing. Just to give one example, Wolff (2012, p. 23) writes:

Where did the borrowing [of the middle class] go? Some have asserted that it went to invest in stocks [this is what you claim]. However, if this were the case, then stocks as a share of total assets would have increased over this period, which it did not (…) Moreover, they did not go into other assets. In fact, the rise in housing prices almost fully explains the increase in the net worth of the middle class (…) Instead, it appears that middle class households, experiencing stagnating incomes, expanded their debt in order to finance normal consumption expenditures.

In our Strategic Analysis last year we provide further evidence towards that direction (see pages 5-10).

Would the situation have been different if inflation was higher, or if the interest rates had not increased in the early 1980s? Most probably it would have (especially if we ignore the complications of inflation on the foreign position of the economy).

At the same time, given the current situation the only way for consumption and private expenditure to pick up is for households to start borrowing again and to increase their debt-to-income ratios. This is based both on economic principle and historical record and we will obviously keep saying it.

The robust recovery in auto sales since the bottom has been one of the few bright spots in the economy. Growth in durables has been as good or better than in the early-to-mid-2000s:

https://www.frbatlanta.org/research/-/media/C7B00E5056E74D2CB7F7DD9399DD0BD6.ashx

I think it’s a pretty safe bet that easy credit availability ( too easy ? ) was a critical factor :

http://houseofdebt.org/2014/06/13/subprime-lending-drives-spending.html

The flip side of the auto sales story is home sales / construction. All we need is another tidal wave of liar’s loans , and this economy will perk right up , for a while.

BTW , it’s fine to be anti-austerity and all , but it would be nice if progressive economists would occasionally point out that one debt- and deficit-free path to stronger growth runs through a reduction in income inequality , which could be even more effective if combined with gov’t stimulus financed via top-1% wealth taxes.

The Republicans don’t stop promoting their wish lists just because the political climate isn’t perfect. Look at the “Death Tax” ( and look quick , because it might disappear at any moment ).