A New Stock-Flow Model for Greece Shows the Worst Is Yet to Come

Dimitri Papadimitriou, Gennaro Zezza, and Michalis Nikiforos have put together a stock-flow consistent model for Greece in order to analyze the path of that nation’s struggling economy and assess alternatives to reigning austerity policies. This is a macroeconomic model based on the New Cambridge approach of Wynne Godley and is the same sort of model used for the Levy Institute’s US strategic analysis series.

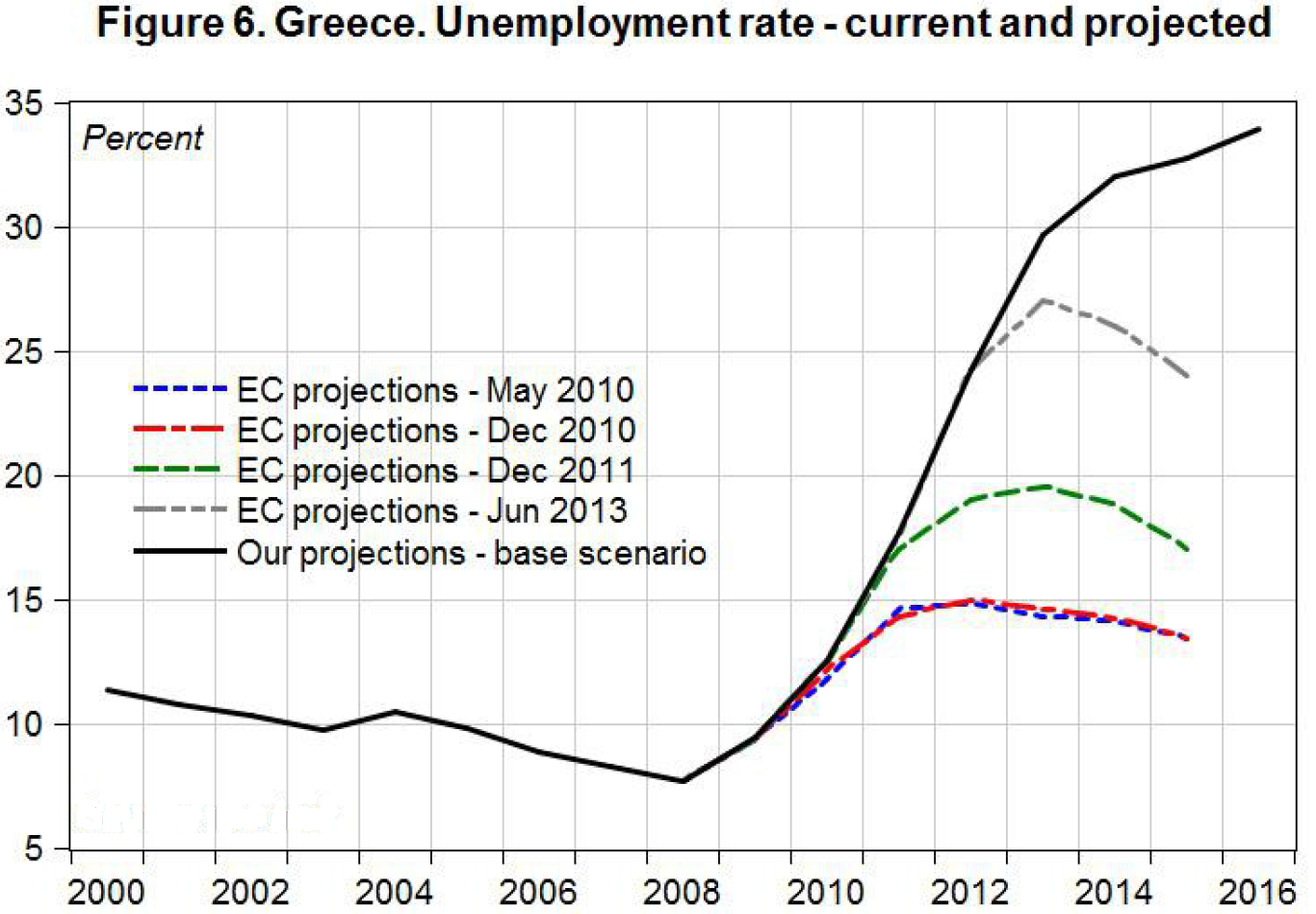

One thing the results of their simulations make clear is that the European Commission (EC) and International Monetary Fund (IMF) have been consistently too optimistic about the Greek economy and the effects of continuing with austerity policies — and still are, even after the IMF’s admission that it had overestimated the benefits of fiscal contraction. Here, for instance, are the EC’s past and current projections for Greek unemployment, compared to the actual results and the Levy Institute’s projections through 2016.

As you’ll notice, the baseline projection generated by the Levy Institute model for Greece (LIMG) shows a rather more dire path for unemployment going forward, compared to the EC’s latest projections. If current policies continue, the unemployment rate could rise from its ruinous 27.4 percent to almost 34 percent by the end of 2016.

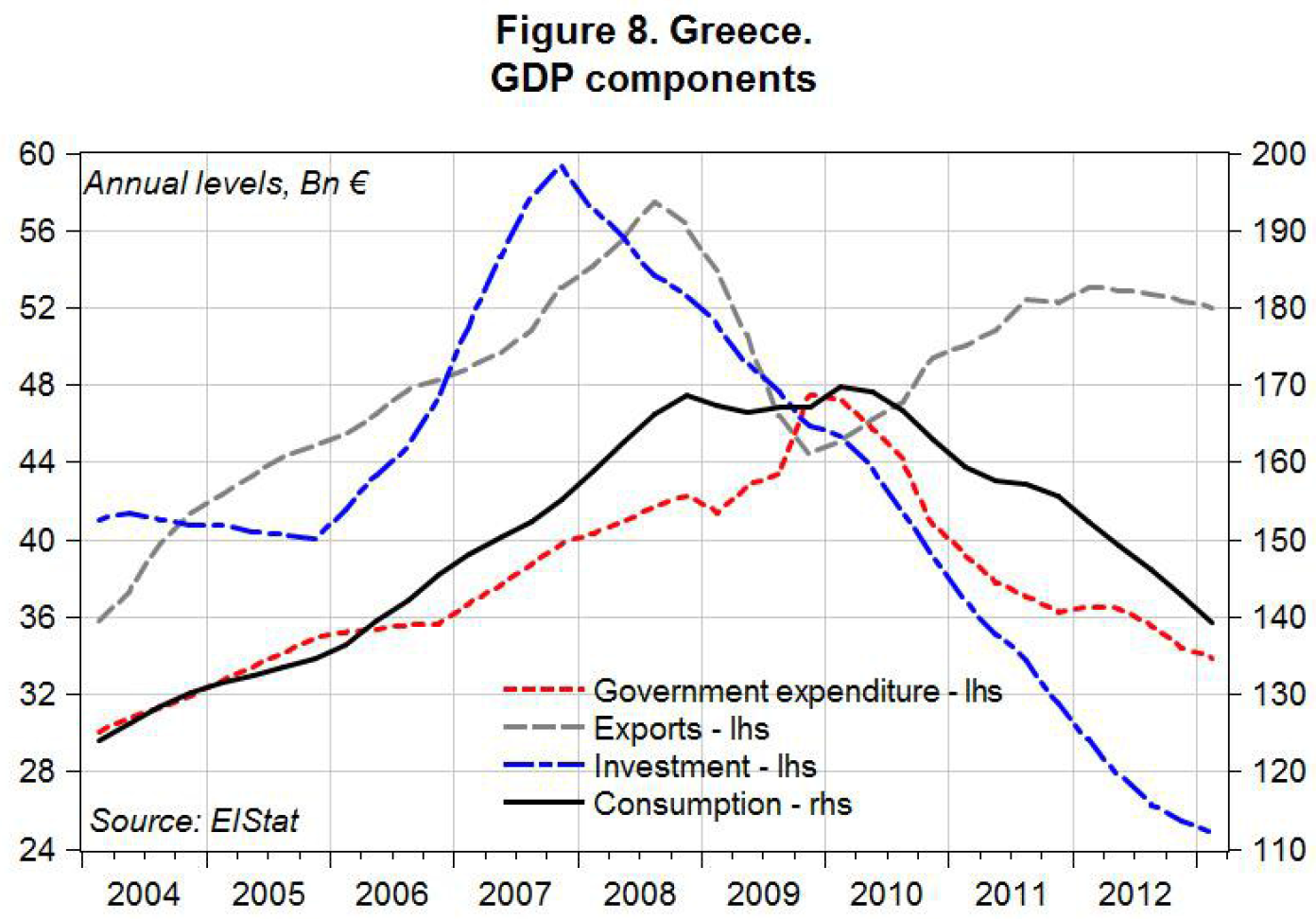

The troika’s (EC/IMF/ECB) “internal devaluation” strategy — based on the idea that forcing a reduction in wages will increase competitiveness and boost export-led growth — isn’t faring well. Cutting wages by government fiat has contributed to a drop in domestic consumption. And as you can see below, while there was an increase in Greek exports that accompanied the onset of fiscal contraction, exports have not risen by nearly enough to compensate for the decrease in the other components of aggregate demand (from their trough, exports grew by almost 8 billion euros; over the same period, government expenditure alone fell by 13 billion euros).

The authors acknowledge that it’s possible exports could grow further, but it’s unlikely that the increase in net exports will be sufficient to make up for plummeting investment, consumption, and government expenditure (and the latest data show that Greek exports were actually declining in the last quarter of 2012). “The implication of our findings,” they conclude, “is that achieving growth in exports through internal devaluation will take a very long time, and furthermore, declining fortunes of the country’s major trading partners do not bode well for [Greece’s] exports.”

The troika’s continued devotion to faulty intellectual doctrines creates serious contradictions in terms of its deficit targets for Greece and its attendant expectations for growth and employment. This new stock-flow model for the Greek economy makes that all the more evident: the authors show that a fiscal stimulus worth around 41 billion euros would be necessary for Greece to reach the troika’s GDP target for the middle of 2016. That would require Greece’s deficit to rise to 12 percent of GDP. Needless to say, that amount — or any amount — of fiscal stimulus isn’t in the troika’s plans.

Papadimitriou, Nikiforos, and Zezza call for a “Marshall plan” for Greece: an investment, funded by the European Investment Bank (EIB), in an expanded public service job creation program — a program that has had impressive results in other countries and, on a smaller scale, in Greece itself.

The strategic analysis for Greece (download an early look at the full report here) is accompanied by a technical report that explains the specification of the model and discusses in more detail how the data were used.

ShareThis

ShareThis

Export growth in Greece can be traced largely to petrol. Local refineries export their production to Bulgaria and nearby countries only to import them back for tax purposes

Dear Mr Karatsoris, what you wrote about Greek-produced petrol being exported to Bulgaria and re-imported, “for tax purposes”, is without substance. Bulgaria is a member of the E.U. There are no longer tariffs and fees charged for trade between the two countries and there can be no question about tax evasion either, since there is now full transparency.

Your point also distracts from the excellent points made above in the article.

Dear Mr Serafimakis, there is your answer moths later from the same site:

“… but if we decompose exports of goods using the Eurostat database by SITC categories, we learn that most – if not all – of the increase in exports of goods is related to oil products(3). Indeed, recent news indicates a fall in non-oil exports.”

from http://multiplier-effect.org/?p=9974

At some point you will also come to realize that our main export markets for oil are Bulgaria and the Balkans and whether you like it or not there is tax evasion…as for your comment that my comment is irrelevant, I was refering to to the authors “The authors acknowledge that it’s possible exports could grow further, but it’s unlikely that the increase in net exports will be sufficient to make up for plummeting investment, consumption, and government expenditure (and the latest data show that Greek exports were actually declining in the last quarter of 2012). “The implication of our findings,” they conclude, “is that achieving growth in exports through internal devaluation will take a very long time, and furthermore, declining fortunes of the country’s major trading partners do not bode well for [Greece’s] exports.”

Goodbye

All EC projections from 2010 on have been made intentionally wrong.

Always higher when lower was needed; always lower when higher scores would have been for the welfare of Greece and similar nations in Europe.

EC projections are tools in the War on Labour-costs, ultimate flexabilization of the quantity and qualitiy of work available in the 27 EU States and preceding empoverishment of the (non)working labour-masses on this Continent, by extreme, needless and not substantiated austerity programs here.

This war is of course an ongoing one, which is already paying off in the country originating all of this, our, troubles.Having 1 of 6 of your citizens( 47,5 million total) on foodstamps programs, must sound and feel like heaven to the Tea Party Republicans and Conservative Democrats.

This is a nearly ideal situation to create for the increasing upflow of money from lower and middle income to the rich getting richer every year.Just “Suck them dry”!

And why limit ourselves to just one Continent.There is much more to be grabbed.So a `Crisis` is created,with big help of Lehman Brothers, and

the system is exported to Europe, tackling the weakest countries first.

Greece functioned as the well known canary in the the EU coalmine.With big, spectacular succeses.

The rest will follow, with the help of above/mentioned fiddled figures.

[…] can read here a new Levy institute study which predicts that unemployment in Greece will go up to 34% if keep doing this (this model is […]

[…] If Greece was Germany, global leaders would not agree to such austerity because they would fear the political repercussions. But this is little Greece. It may have been a superpower 2,500 year ago, but Alexander is dead, Sparta defeated, and the TROIKA vents its fury like the Titans escaped from Hades. For more see: A New Stock-Flow Model for Greece Shows the Worst is Yet to come […]