Of Voices in the Air and Never-Ending Dreams of Helicopter Drops

Confusions about so-called helicopter money (HM) continue unabated. My recent letter to the editor of The Financial Times, titled “’Helicopter money’ is a muddled fiscal policy by another name,” has not met with universal approval. In fact, it seems to have ruffled some feathers and caused some annoyance.

Simon Wren-Lewis is a case in point. In a response to my letter (and a piece in the FT by John Kay) published on the Mainly Macro blog, Wren-Lewis reiterates his concerns that trying to distinguish fiscal from monetary policies is ultimately pointless and that central banks need to have HM in their armory since otherwise delegating stabilization would be dangerously incomplete. Mr. Wren-Lewis is perhaps best known for his selfless efforts at trying to wring any sense out of mainstream macroeconomics – an endeavor that takes a lot of wringing indeed. Another case in point is fellow helicopter warrior J. Bradford DeLong, who re-published Wren-Lewis’s HM elaborations on his own blog with the remark “intellectual garbage collection.” The wisdom of HM is just too obvious to be challenged, it seems.

But first recall here that Bradford DeLong is the supposedly “New Keynesian” macroeconomist who a few years back published a piece titled “The Triumph of Monetarism?” in the Journal of Economic Perspectives, arguing – quite correctly actually! – that New Keynesianism was really muddled New Monetarism by another name. It is also the same new monetarist economist who not so long ago published a piece together with Larry Summers titled “Fiscal Policy in a Depressed Economy,” in which the two argued that the time was right for governments to ramp up their investment spending and not worry about debt. That argument made quite a bit of sense to me at the time – and it still does today, as I suggested in my FT letter.

In any case, I was quite amused when at an event at the Brookings Institution on May 23 Larry Summers proclaimed that: “Helicopter money, hear me, helicopter money is fiscal policy. There is no such thing as helicopter money that isn’t fiscal policy.” That may well be just yet another useless point to make of course. But I will leave it to Messrs. Wren-Lewis and DeLong to do the intellectual garbage sorting of Mr. Summers’ remark.

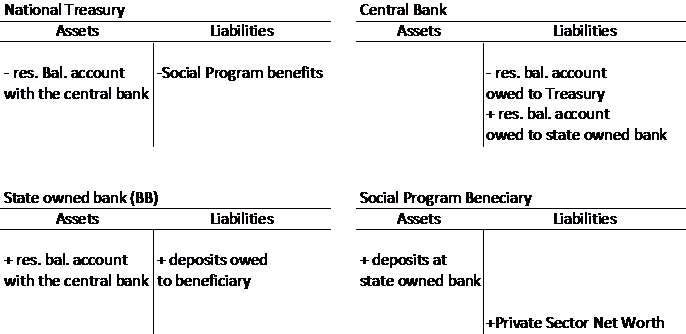

Moving on, a rather interesting piece was published on VoxEU by Claudio Borio (together with Piti Disyatat and Anna Zabei). Borio’s earlier research at the BIS focused on central banks’ operating procedures. He isn’t someone who can be easily fooled about what central banks are doing or not doing. Furthermore, and this may not be a coincidence, he is also one of those rare cases among monetary economists who clearly identified what I long ago dubbed the “loanable funds fallacy” in Ben Bernanke’s “saving glut hypothesis” (see here). continue reading…

ShareThis

ShareThis