A Nonbehavioral Theory of Saving

Michalis Nikiforos

“We present a model where the saving rate of the household sector, especially households at the bottom of the income distribution, becomes the endogenous variable that adjusts in order for full employment to be maintained over time. An increase in income inequality and the current account deficit and a consolidation of the government budget lead to a decrease in the saving rate of the household sector. Such a process is unsustainable because it leads to an increase in the household debt-to-income ratio, and maintaining it depends on some sort of asset bubble. This framework allows us to better understand the factors that led to the Great Recession and the dilemma of a repeat of this kind of unsustainable process or secular stagnation. Sustainable growth requires a decrease in income inequality, an improvement in the external position, and a relaxation of the fiscal stance of the government.”

Is a Very High Public Debt a Problem?

Pedro Leão

“we propose a policy architecture that differs from [Abba] Lerner’s in two aspects: it envisions a different way of preventing a very high public debt from ending in default, and it eliminates the burden associated with levying taxes to meet the interest payments on the debt (in one word, it eliminates the debt burden altogether). Our architecture requires flexible exchange rates. It involves (i) having the central bank impose near-zero nominal government bond yields for as long as necessary—a stance that should be accompanied by (ii) a replacement of monetary by fiscal policy as the instrument to control inflation.

A second objective of this paper is to show that government deficits associated with a full-employment fiscal policy do not face a financing problem. After these deficits are initially financed through the net creation of base money, the private sector’s savings always come in the form of government bond purchases or, if a default is feared, of ‘acquisitions’ of new money.”

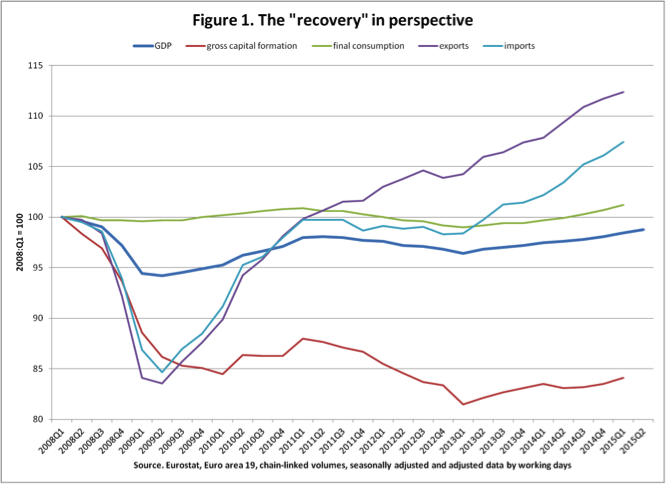

Making the Euro Viable: The Euro Treasury Plan

Jörg Bibow

“The idea is to create a Euro Treasury as a vehicle to pool future eurozone public investment spending and have it funded by proper eurozone treasury securities. Member state governments would agree on the initial volume of common area-wide public investment spending and on the annual growth rate of public investment thereafter. Beyond that, the Euro Treasury operates on auto-pilot. … This is not simply another ‘euro bonds’ proposal, though. In particular, there is no debt mutualization of existing national debts involved here. Member states alone would remain responsible for their respective national public debt. …

As to the evolution of national public debts under the Euro Treasury plan, steady deficit spending on public investment funded at the center that is the basis of Europe’s common future will finally allow and enable national treasuries to (nearly) balance their structural current budgets. Within one generation, there will be little national public debt left to worry about. … In general, member states will experience a decline in their overall interest burden as cheaper debts replace more expensive debts over time. While mimicking the original Maastricht criteria of fiscal rectitude and stability at the union level, the overall outcome would also resemble the situation in another—functioning—currency union during normal times: the United States.”

Marx’s Theory of Money and 21st-century Macrodynamics

Tai Young-Taft

“Marx’s theory of money is critiqued relative to the advent of fiat and electronic currencies and the development of financial markets. Specific topics of concern include (1) today’s identity of the money commodity, (2) possible heterogeneity of the money commodity, (3) the categories of land and rent as they pertain to the financial economy, (4) valuation of derivative securities, and (5) strategies for modeling, predicting, and controlling production and exchange of the money commodity and their interface with the real economy.”

The Effects of a Euro Exit on Growth, Employment, and Wages

Riccardo Realfonzo and Angelantonio Viscione

“A technical analysis shows that the doomsayers who support the euro at all costs and those who naively theorize that a single currency is the root of all evil are both wrong. A euro exit could be a way of getting back to growth, but at the same time it would entail serious risks, especially for wage earners. The most important lesson we can learn from the experience of the past is that the outcome, in terms of growth, distribution, and employment, depends on how a country remains in the euro; or, in the case of a euro exit, on the quality of the economic policies that are put in place once the country regains control of monetary and fiscal matters, rather than on abandoning the old exchange system as such. …

Although the exit from a monetary union such the eurozone would be unprecedented, some important pointers can be found in the currency crises of the past that more closely resemble the present case. For this purpose, we will examine the currency crises that in recent history have entailed large devaluations of the exchange rate and that were accompanied by the abandoning of previous agreements or exchange systems. This allows us to take into account both the phenomenon of devaluation and the political-institutional changes that follow when exchanges regimes are abandoned.”

ShareThis

ShareThis