Bubbles and Piketty: An Interview with L. Randall Wray

L. Randall Wray appeared on Thom Hartmann’s radio show yesterday for a lengthy and wide-ranging interview:

L. Randall Wray appeared on Thom Hartmann’s radio show yesterday for a lengthy and wide-ranging interview:

On reading a recent post by Ed Dolan at Economonitor with some evidence of the lack of a strong Phillips relationship for consumer-price inflation in US data, it occurred to me to try a measure of total compensation per hour with recent data. The wage relationship estimated over all available quarters, using averaged monthly observations for the civilian unemployment rate, is shown above, with a scatter plot and an estimated regression line. Like the relationship estimated by Dolan, the regression line above suffers from a rather loose fit (constant: 6.87; slope coefficient: -.29; R-squared = .02). A complete explanation of inflation is complicated and of course also involves other costs, including raw materials such as fuel. The latter costs are subject of course to “cost-push”-type inflation at times, as are wages. Exchange rates of course affect these costs.

A time series graph below displays both series over the entire sample period, 1948q1 to 2014q1. As some have observed, the exceedingly high unemployment rates of the post-financial-crisis era (blue line) have resulted in very weak or negative compensation growth rates (red line). The latter are not adjusted for inflation in the figures, since we are focusing on nominal data in this post. The downward trend in nominal wage growth in the right side of the figure (red line) helps to explain recent declines in the so-called wage share, which measures the fraction of national income going to labor costs. (However, see this New York Times article for some evidence that falling unemployment is beginning to bring some inflation-adjusted wage growth to parts of the US.)

By the way, if inflation were to become a large problem (and it seems well-contained now), non-recessionary methods exist to try to alleviate it. Even where the Phillips-curve relationship is strong, the human costs of using it to combat inflation are usually very high, given the existence of alternative policies that could perhaps be given a try in the US.

In a new policy brief, Jan Kregel looks at a lesser-known, early period of Minsky’s work on financial reform. In the ’60s, Minsky was a consultant to a number of government agencies, including the Federal Reserve, on issues related to financial regulation. In this context, he came up with a new approach to bank examination, which he called “cash-flow based.” The new approach evaluated bank liquidity, not as an innate feature of a particular class of assets, but as a function of the balance sheet of the institutions under examination, the markets for those assets, the state of the macroeconomy and the financial system as a whole, and much else. In fact, as Kregel explains, what Minsky was after here was related to an early form of what we now call “macroprudential regulation.”

The evolution of Minsky’s thought on this approach to bank examination is interesting enough in itself, but it’s also a reflection of Minsky’s broader thinking about financial regulation and reform. Minsky developed his regulatory proposals in the ’60s and ’70s with an eye to what was to become his well-known “financial instability hypothesis,” which is to say, his proposals were informed by a theory of endogenous financial instability: a theory in which financial crises are not only possible, but are to be expected; generated as a result of the “normal” functioning of the financial system. Without such a theory, as Kregel points out, it’s hard to formulate effective regulation:

As Minsky was fond of pointing out, the bedrock of mainstream theory is a system of self-adjusting equilibrium that provides little scope for the discussion of a systemic crisis, since, in this theory, one could not occur. It was thus extremely difficult to formulate prudential regulations to respond to a financial crisis if one could only occur as the result of random, external shocks, or what Alan Greenspan would consider idiosyncratic, nonrational (fraudulent) behavior. The only basis for regulation would be to concentrate on the eradication of the disruptive behavior of bad actors or mismanaged financial institutions. From this initial presumption, the formulation of regulations and supervisory procedures required the assessment of the activities of individual banks—without any reference to their relations with other institutions or the overall environment in which they functioned.

One consequence of being informed by a proper theory of financial instability, Minsky maintained, is that regulation has to be responsive to innovations in the financial system; innovations that are often reactions to new regulatory frameworks. What this calls for, then, is not just the right set of rules, whether your preferred model is Glass-Steagall or something else, but also an adaptive, “dynamic” framework that’s attuned to the evolution of the financial system. This is from the preface:

the challenge for reform is not just the proper formulation and implementation of specific rules, but the development of an approach that is sensitive to the potential of actors in the financial system to adapt and innovate, creating new practices that threaten the stability of the system in ways that may not become apparent until the next crisis hits. Financial regulation and examination procedures need to be constantly reassessed in order to avoid becoming obsolete. And in that sense, as Minsky recognized, “the quest to get money and finance right may be a never ending struggle.”

There’s a lot more here, including Kregel’s take on the ongoing debates about imposing specific capital and liquidity ratios on financial institutions:

While the imposition of minimum liquidity and capital ratios is an improvement over the prior risk-based approach, such target ratios are not macroprudential regulations in Minsky’s sense. Similarly, stress tests of banks’ capital positions are applied to banks individually, rather than in a systemic interaction. Neither approach to macroprudential regulation takes into account the dynamic macro factors that impact the bank’s position-making assets and liabilities and the secondary markets in which they trade, or the ongoing institutional and policy changes that are a natural part of the economic system.

Download it here: “Minsky and Dynamic Macroprudential Regulation“

For those of you who haven’t seen it already, Duncan Weldon did a feature on Hyman Minsky for the BBC last week, including this short article and a 30-minute piece for BBC radio.

In the radio segment, Adair Turner says this about Minsky’s contribution and his departure from the mainstream (a description of the pre-crisis orthodoxy which is probably baffling to many unfamiliar with the field):

“The dominant strain of modern economics had assumed, before the crisis, that you could largely ignore the details of the financial system and banks in particular. The phrase that was used was that finance was simply a sort of veil through which relationships between savers and borrowers passed and it didn’t have an influence, and at the … core of Minsky’s analysis is the fact that financing contracts and banks in particular have a crucial influence.”

Weldon devotes a great deal of the program to the “financial instability hypothesis,” for which Minsky is, perhaps, best known, but Minsky also offered an approach to re-regulating the financial system that makes his work as useful as a prescription for a more stable capitalism as it is as a diagnosis of financial crises. (The Levy Institute’s short ebook, Beyond the Minsky Moment (pdf), includes a survey of Minsky’s views about how to reconstitute the financial structure and explains why Dodd-Frank falls well short. The Minsky archive has also been digitized to provide access to many of Minsky’s unpublished papers and notes.)

The annual conference inspired by Minsky’s work will be held at the National Press Club in Washington, DC next week.

I recently did an interview for the magazine “Synchrona Themata” (“Contemporary Issues”). The interview, which will appear in Greek, was conducted by Christos Pierros, doctoral student at the University of Athens Doctoral Program in Economics (UADPhilEcon). What follows is the English transcript:

What do you think went wrong in 2008? Why was standard macro theory unable to predict such an event?

This was a collapse of what Hyman Minsky called “Money Manager Capitalism.” In many ways it was similar to the 1929 collapse of “Finance Capitalism” that led to the Great Depression. MMC and FC share several common characteristics. First, the dominant approach of economists and policy makers in the 1920s and in the 2000s was one of “laissez faire”—that is, a worship of free markets. Importantly, that meant that finance was “freed” from regulation and supervision. Second, in both cases we lived in an era of globalization—with both goods and finance crossing borders fairly freely. That ensured that when crisis hit, it would spread around the world. Third, finance dominated over industry. Our economy in both cases was “financialized”—with finance sucking 40 percent of all corporate profits out of the economy. To say that “finance ran amuck” is an understatement. To say that our economies were completely taken over by “blood sucking vampire squids of Wall Street” is only a slight exaggeration.

Standard macro theory either thinks all these are “good” trends, or ignores them. That is why—as the Queen of England remarked—none of these economists saw the crisis coming.

Do you believe that by using other tools of analysis (another methodology) one could have seen it coming? If yes, which type of analysis would that be?

Certainly. Many of us saw the crisis coming. The three approaches that made it possible to understand what was going on were: a) Minsky’s financial instability approach; b) Wynne Godley’s sectoral balance approach; and c) Modern Money Theory—which actually builds upon the approaches of Minsky and Godley. All of those working in these approaches “saw it coming.”

Just very briefly, those following Minsky could see that financial institutions were engaged in highly risky practices that would eventually cause liquidity and solvency problems. Those following Godley knew that government budgets were too tight—including the governments of the USA, Spain, and Ireland. By the same token, private sector households and firms had taken on far too much debt. That was particularly true of homebuyers in the USA, in the UK, and in Spain. And those following MMT knew that Euroland was designed to fail; by disconnecting fiscal policy from currency sovereignty, the EMU ensured that the first serious downturn or financial crisis would threaten the very existence of the European Union.

Do you see any shift in the paradigm of economics taking place? If yes, towards which direction? continue reading…

From the preface to a new policy brief by Amit Bhaduri:

In our era of global finance, the theory of aggregate demand management is alive and unwell. In this policy brief, Bhaduri describes what he regards as a prevalent contemporary approach to demand management. Detached from its Keynesian roots, this “vulgar” version of demand management theory is being used to justify policies that stand in stark contrast to those prescribed by the original Keynesian model. Rising asset prices and private-debt-fueled consumption play the starring roles, while fiscal policy retreats into the background. …

While some might insist that the age of global finance leaves little room for the idea of demand management, Bhaduri contends that the theory survives, but that it does so in a form that is nearly unrecognizable from the original. This contemporary model of demand management receives its inspiration from the presuppositions of neoclassical economics, and its policy emphasis is often the very opposite of the old Keynesian model. … To support demand, the “vulgar,” or “Great Moderation,” model hinges on the interplay between expectations of ever-rising asset prices and a consumption boom driven by private debt.

Bhaduri cautions, however, that a model centered on private credit creation is prone to instability. More and more financial investment is needed to produce greater returns and boost asset prices, continually shifting the composition of investment from the real to the financial and creating the conditions for a delinking of finance from output and employment. When the paths of the financial and real sectors of the economy diverge, when incomes stagnate while debt and asset prices continue to rise, this creates the conditions for a financial crisis.

Read the brief here.

C. J. Polychroniou:

A strong case can be made that what we have been witnessing since [2007-08] is not simply a severe financial crisis centered in the developed world but the fact that today’s capitalism is simply incapable of functioning in an economic way conducive to maintaining sustainable and balanced growth.

The so-called “financialization” of the economy, so prone to financial crises and meltdowns as the late Hyman Minsky has shown, cannot be understood independent of the production processes or developments in the real economy. Advanced capitalism had been facing severe structural stresses, strains and deformations — including overproduction, trade deficits, lack of job growth and elevated public and private debt levels — for quite a few decades prior to the eruption of the financial crisis of 2007-08.

Indeed, the “financialization” wave — which many have labeled “casino capitalism” or “stock market capitalism” but which amounts essentially to the deregulation of giant financial entities capable of shaping and controlling the fate of national economies — began as a result of the structural problems associated with the postwar regime of capital accumulation, whose collapse in the mid-1970s threatened the growing expansion of capitalism. Thus, “financialization” does not spring out of the blue but emerges as an alternative model to the decay of the postwar regime of accumulation.

Read the rest here.

Is the U.S. economy heading towards another bubble? Since last week, the number of commentators on this subject has been growing, from Robert Shiller to Nouriel Roubini (on housing markets).

In our first chart we report the Standard & Poor’s 500 stock market index, normalized by a consumer price index to remove the common trend in prices. Our measure has increased by 105.6 percent from its most recent bottom in March 2009. In the previous rally, which started from a bottom value in February 2003, the index increased by only 63 percent before the start of a rapid descent in July 2007.

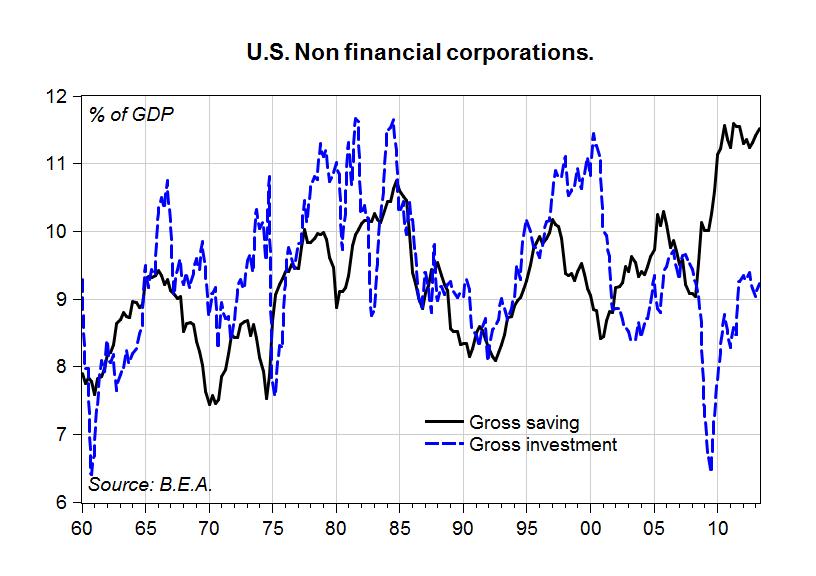

Is a buoyant stock market justified by expected profitability? In the next chart, we report gross saving of non-financial corporations – that is, undistributed profits gross of capital consumption – scaled by GDP, along with gross investment (which includes changes in inventories). All figures are computed from the Integrated Macroeconomic Accounts published by the B.E.A.

The chart clearly shows that profits have reached an all-time high at 11.5 percent of GDP, compared to an average of 9 percent over the 1960-2007 period. If current profits are the basis for expected future profitability, our data suggest that the stock market rally is justified. But is this trend stable and sustainable?

The chart also shows what we may call an investment gap. While profits and investment have usually moved in line, it was usually the case that investment exceeded retained profits. But since the second half of 2008, profits have soared while investment dropped, opening a gap which is currently over 2 percent of GDP. A low level of investment is not a good sign for future growth.

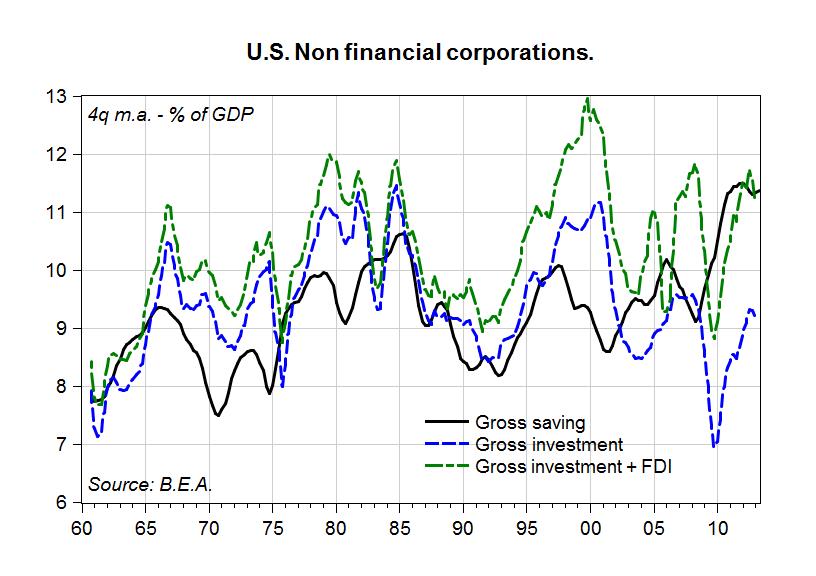

What are companies doing with such exceptional profits? In the next chart we add U.S. foreign direct investment (FDI) made abroad to domestic investment in our previous chart (while at the same time switching to moving averages to reduce the volatility of quarterly FDI).

The new chart is suggesting that foreign direct investment is a major destination for retained profits, and that FDI did not suffer the same downturn seen in domestic investment during the last recession.

Data from the B.E.A. on the composition and direction of U.S. FDI show it is difficult to evaluate where U.S. foreign direct investment is directed. While data for FDI in manufacturing show the emerging role of China as recipient of U.S. FDI, its weight is still below 5 percent of total FDI in manufacturing. Besides, the share of manufacturing in total FDI in 2012 is only 14 percent, while multinational companies, classified as “Holding Companies (non bank)” in B.E.A. statistics, account for almost 44 percent of total FDI in 2012. Countries receiving FDI in this grouping seem to be financial centers: the Netherlands (25.6 percent), Luxembourg (15.5 percent), Bermuda (11.2 percent), and the U.K. (10.7 percent).

Summing up, our findings suggest that U.S. non-financial corporations are in a healthy state – as measured by their net profits – but that this will not necessarily imply stronger U.S. growth and job creation. On the contrary, the data are coherent with a further increase in the concentration of income leading to financial speculation, in the U.S. as well as in foreign financial markets.

Restoring jobs and prosperity in the U.S. does not seem to be what U.S. corporations are working towards, and yes, the soaring stock market may change course very quickly, if “financial markets” make this decision.

Restoring sustainable growth in the U.S. (and elsewhere) requires a reversal of the trend in income distribution, since, as Stockhammer reminds us, “rising inequality has increased the propensity to speculate as richer households tend to hold riskier financial assets than other groups,” and “higher inequality has led to higher household debt as working class families have tried to keep up with social consumption norms despite stagnating or falling real wages” – a fact we already investigated a few years ago.

A new issue of Accounting, Economics and Law has published a series of articles (open access) on Minsky and banking. In addition to my contribution, you can find some nice pieces by Thorvald Moe, Yuri Bondi, and Robert Boyer.

According to Minsky, “A capitalist economy can be described by a set of interrelated balance sheets and income statements”. The assets on a balance sheet are either financial or real, held to yield income or to be sold or pledged. The liabilities represent a prior commitment to make payments on demand, on a specified date, or when some contingency occurs. Assets and liabilities are denominated in the money of account, and the excess of the value of assets over the value of liabilities is counted as nominal net worth. All economic units – households, firms, financial institutions, governments – take positions in assets by issuing liabilities, with margins of safety maintained for protection. One margin of safety is the excess of income expected to be generated by ownership of assets over the payment commitments entailed in the liabilities. Another is net worth – for a given expected income stream, the greater the value of assets relative to liabilities, the greater the margin of safety. And still another is the liquidity of the position: if assets can be sold quickly or pledged as collateral in a loan, the margin of safety is bigger. Of course, in the aggregate all financial assets and liabilities net to zero, with only real assets representing aggregate net worth. These three types of margins of safety are individually important, and are complements not substitutes.

If the time duration of assets exceeds that of liabilities for any unit, then positions must be continually refinanced. This requires “the normal functioning of various markets, including dependable fall-back markets in case the usual refinancing channels break down or become ‘too’ expensive”. If disruption occurs, economic units that require continual access to refinancing will try to “make position” by “selling out position” – selling assets to meet cash commitments. Since financial assets and liabilities net to zero, the dynamic of a generalized sell-off is to drive asset prices towards zero, what Irving Fisher called a debt deflation process. (To some extent, this can be called a liquidity problem – but it is really more than that. I’ll return to this later.) Specialist financial institutions can try to protect markets by standing ready to purchase or lend against assets, preventing prices from falling. However, they will be overwhelmed by a contagion, thus, will close up shop and refuse to provide finance. For this reason, central bank interventions are required to protect at least some financial institutions by temporarily providing finance through lender of last resort facilities. As the creator of the high-powered money, only the government – central bank plus treasury – can purchase or lend against assets without limit, providing an infinitely elastic supply of high-powered money.

These are general statements applicable to all kinds of economic units. continue reading…

As is well known, Hyman Minsky was a student of Joseph Schumpeter’s at Harvard. Minsky’s “stages” theory of capitalist development, fleshed out during the later part of his life while he was here at the Levy Institute, arguably owes something to the influence of his former dissertation adviser. There’s a short paper in the archive from 1992, “Schumpeter and Finance” (pdf), in which Minsky presents a tight, clear summary of his vision of the evolution of capitalism and finance, right up to the present-day stage of “money manager capitalism.”

You should read it for that reason alone (especially if your acquaintance with Minsky’s work extends only to his “financial instability hypothesis”), but it also contains a short passage that deserves to be quoted on its own, in which Minsky, in the context of a reminiscence of his teacher (“We talked about important things as well as about economics”), insists on the need to approach economics as the study of an “evolutionary beast”:

“In 1948–49 the representative graduate student considered Schumpeter to be passé. Paying attention to him, joining him in his study was evidence of a lack of fundamental seriousness, of dilettantism. Given the command of mathematics that economists of that time possessed, Schumpeter’s model was not tractable. As a result his vision was ignored by the candidates striving to be mathematical economists and econometricians.

The events of our time, especially but not exclusively the break-up of the Soviet ministerial model of socialism, vindicates the Schumpeter vision of economies as evolving systems, systems that exist in history and change in response to endogenous factors. (Schumpeter acknowledged that this vision owes much to Marx.) This message, that societies are evolutionary beasts which cannot be frozen in time and reduced to static mathematical formulations, was never more relevant that it is today. No doctrine, no vision that reduces economics to the study of equilibrium seeking and sustaining systems can have a long-lasting relevance. The message of Schumpeter is that history does not lead to an end of history.”

ShareThis

ShareThis