Michael Stephens | February 16, 2012

The people at Bloomberg appear to have made a curious error on their website yesterday. They have attributed an op-ed to Amity Shlaes that was almost certainly not written by her. You see, Amity Shlaes is a well-known skeptic of Keynes and all things Keynesian, having written the bible for those who like to claim that the New Deal made the Great Depression worse. (For a nice takedown of such claims, as well as Shlaes’ contributions in particular, see this Levy Institute policy brief.)

The Bloomberg op-ed in question contends that the Obama administration’s intention to withdraw militarily from Afghanistan and other places will devastate those countries’ economies. This is because, according to the op-ed, establishing US military bases in foreign countries boosts economic growth there.

The real Amity Shlaes would have carefully instructed us that such public interventions not only cannot increase economic growth (even in the context of a downturn) but will actually decrease it (the New Deal, you see, is what made the regular ol’ Depression “Great”).

Now if this was written by Amity Shlaes, it is a peculiar way of announcing her conversion. But let’s not quibble over ceremony. If it is indeed Shlaes, let’s follow her lead. In order to boost the growth rate in a time of economic malaise here at home, we should invite the US military to occupy the United States; we could even pay them a bonus to do it (Shlaes’ calculations suggest this might still be worth our while).

But if the military is too busy increasing other countries’ growth rates, I have another idea. We could initiate an emergency recruitment drive for the US Army and station the new troops here in the United States, carrying out nation building in particularly distressed economic regions (there are, I believe, a few million people without jobs who would welcome the opportunity). Of course we might need to build some new infrastructure bases to facilitate these operations here in the US, and may have to hire some additional support staff.

And if the threat of being shipped overseas and put in harm’s way is a barrier to recruitment, we could always create a new, strictly domestic branch of the military that recruits civilians to engage in nation building through repairing schools and providing social services. We could call it, I don’t know, the Civilian Conservation Nation Building Corps, or something like that. But none of that Keynesian nonsense please.

Comments

Michael Stephens | February 10, 2012

No matter what happens on Sunday, when the Greek parliament is scheduled to vote on the latest bailout package, on Monday Greece will wake up in the grip of an employment crisis (20 percent unemployment, with a near 40 percent youth unemployment rate). In the Huffington Post Dimitri Papadimitriou tells us what we can (and can’t) do about it.

Depending on the Greek private sector alone to produce enough jobs to stave off these socially corrosive levels of unemployment is unrealistic. Drawing from a report on the Greek labor market recently produced by the Levy Institute, Papadimitriou lays out the case for direct public service job creation. As Papadimitriou points out, Greece is currently experimenting with a similar, small-scale version of the idea:

… a better option is being tried on a small scale: A labor department direct public service job creation program with an initial target of 55,000 jobs. Participants are entitled to up to five months of work per year, in projects — implemented by non-governmental organizations — that benefit their communities. A similar, streamlined, Interior department program, this one without NGO participation, will generate up to 120,000 openings.

This approach is the Greek government’s best shot at slowing the nosedive in employment, and at circumventing further catastrophe. The plans have been designed to specifically address and avoid the nepotism, corruption, and favoritism that plague poorly conceived ‘workfare’ schemes. With proper targeting, monitoring, and evaluation as the projects move along, the outcomes should be impressive

Read the whole thing here at HuffPo.

Comments

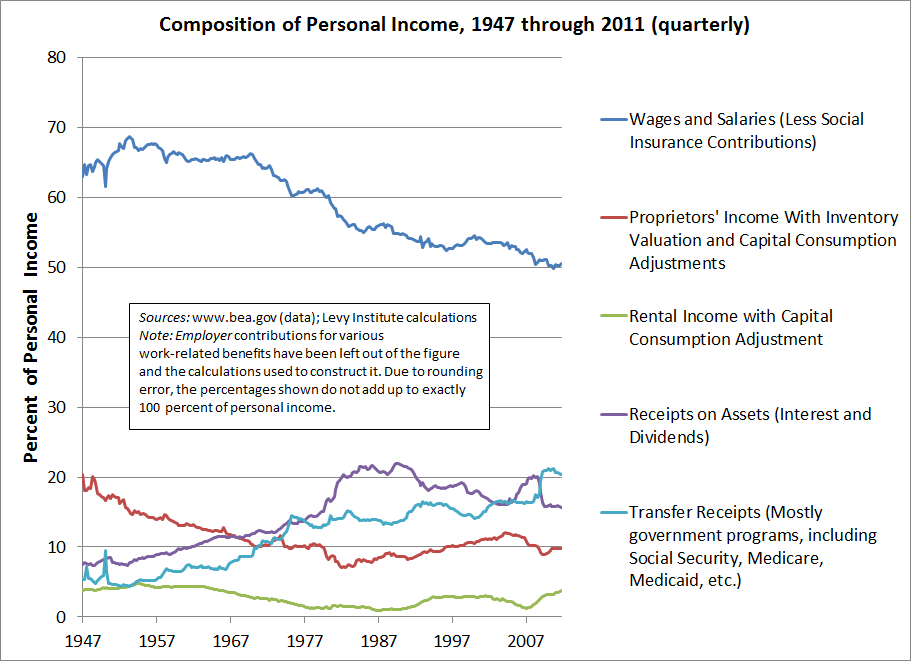

Greg Hannsgen |

(Click to enlarge.)

See the blue line in the upper half of the figure above? That line shows the portion of personal income made up of wage and salary disbursements, as a percentage of total personal income. (As the figure notes, I’ve subtracted social insurance contributions such as Social Security taxes. Also, employer contributions to Social Security, private pensions, etc., have been completely ignored in my calculations.) I have been looking into the possible effects on consumer spending of changes in the composition of income. Please click on figure if you want to see a larger version.

Comments

Michael Stephens | February 8, 2012

The latest chapter in the “why was the original stimulus so small?” story is a memo from December 2008 that reveals Larry Summers’ assessment as to why the stimulus (ARRA) had to be limited to around $800 billion—about half of what was necessary, in Summers’ estimation. There are various conclusions you can draw from this memo, but the aspect I’d like to focus on is this: Larry Summers’ suggestion that $225 billion of “actual spending on priority investments” is all that the government could get out the door over a two year time span (and so the rest had to be made up of tax cuts, aid to states, etc.).

Let’s grant for the sake of argument that Summers is correct about this “shovel ready” figure. The question is: what can we do about it? If you’re looking for short-term results, the answer is probably “not much.” Even things like speeding up environmental impact assessments for infrastructure projects wouldn’t have much effect (at the link, Brad Plumer tells us that only 4 percent of highway infrastructure projects even require such environmental reviews).

But looking ahead, there is more we could and should be doing. Back in 2009 Martin Shubik sketched out a plan in a Levy Institute policy note for creating a “Federal Employment Reserve Authority“—a kind of Fed for employment (yes, I know: the Federal Reserve is the “Fed for employment.” But you don’t need to look very hard to see that the sides of the dual mandate aren’t equally weighted). Among other things, the FERA would maintain state branches that are charged with keeping updated and prioritized lists of potential public works projects (with a preference for self-liquidating projects) and providing constant monitoring and evaluation so that financing can be put in place as soon as unemployment reaches a particular trigger level in that region. Regional public investment would respond to objective employment conditions. continue reading…

Comments

Michael Stephens | February 6, 2012

(click to enlarge)

Comments

Michael Stephens | January 18, 2012

Marshall Auerback compares the job numbers in the US to those in Europe and asks why the US is doing so much better (or failing less miserably). One of the differences he highlights is the zealous dedication to fiscal austerity in Europe, compared to the relatively half-hearted, passive observance of doctrine in the US.

For people operating on the basis of loose stereotypes about the differences between the US and Europe, this has perhaps turned out to be surprising. You might have assumed that Europe’s more expansive social welfare systems would be accompanied by more progressive approaches to fiscal or monetary policy. But as Matt Yglesias observes, Europe is awash in some pretty conservative ideas about macroeconomic policy:

… the American right has lately fallen out of love with both J.M. Keynes’ fiscal stimulus ideas and Milton Friedman’s monetary stimulus ideas. Tussle between these two has dominated practical policymaking for decades in the United States, but if conservatives were to cast their eyes toward Europe they’ll find a continent where these ideas about demand-side management get short shrift.

(To muddy the waters a bit, due in part to the strength of the aforementioned social welfare supports the default fiscal policy stance in Europe is actually more expansionary than in the US. More robust automatic stabilizers in Europe make a “do nothing” policy more fiscally expansionary, even while official or discretionary European policy is dedicated to deficit reduction and tight money. In the US you have almost the reverse: automatic stabilizers play less of a role in counteracting recessions, while official policy—in the White House, if not Congress—continues to feature calls for more discretionary stimulus.)

To add a cute little twist to this tale, the dismal failure of these contractionary policies in Europe could, perversely, help entrench the American right and its ideas for some time. If Europe collapses outright or even continues to limp along, the US recovery is likely to get bogged down, which in turn makes the election of a Republican President in 2012 more likely. And as Ezra Klein points out, if more robust catch-up growth emerges in the US some time in the next five years, the person sitting in the Oval Office, and his policy message, will get most of the credit. So the abysmal practical failure of a set of policy ideas in Europe could actually end up entrenching those same ideas on this side of the pond.

Comments

Michael Stephens | January 13, 2012

Randall Wray passes on this piece by Chris Hayes (of The Nation and MSNBC) on the challenge mounted by heterodox economists to the neoclassical consensus. Reporting from the ASSA, Hayes gets into the ways in which the boundaries of the “mainstream” are policed in economics. It’s really worth reading the whole thing. I particularly liked this bit:

Despite the fact that as many as one in five professional economists belongs to a professional association that might be described as heterodox, the phrase “heterodox economics” has appeared exactly once in the New York Times since 1981. During that same period “intelligent design,” a theory endorsed by not a single published, peer-reviewed piece of scholarship, has appeared 367 times.

Comments

Michael Stephens | January 11, 2012

Over the break an article appeared in The Economist spotlighting three “schools of macroeconomic thought”: Scott Sumner’s market monetarism, Austrian free banking, and neo-chartalism (MMT). In addition to noting the role of the blogosphere in refining and promoting these heterodoxies, the article elects to use Paul Krugman as a stand-in for the “mainstream” opponent.

If you step back, what’s slightly unsatisfactory about this choice is that Krugman is, right now, more in tune with the policy preferences of two-thirds of these “doctrines on the edge of economics” than he is with the reigning fiscal or monetary policy stance of the US government. Krugman has written extensively about the fact that our current debt and deficit levels present no serious current economic problem. (The dispute between Krugman and MMTers stems from disagreements about the long-term debt.) And as The Economist points out, Krugman is fine with nominal GDP targeting.

Figuring out where to draw the boundaries of “the mainstream” in the economics profession is one thing, but when it comes to the range of politically acceptable policy options (a different kind of mainstream, admittedly) Krugman stands shivering in the cold side-by-side with a lot of heterodox thinkers. With respect to both policy outcomes and policy rhetoric, our institutions seem to pay a great deal more attention to deficits, debt, and inflation than they do to unemployment and the threat of deflation (though one might argue that, at least with respect to fiscal stimulus, this has more to do with the fact that in the US political system the “opposition” party has the ability to see the government fail. Resistance to fiscal stimulus may all but disappear from Congress in the event of a Romney presidency. Explaining the preferences of the FOMC is a more complicated affair.) The mainstream policy space since 2010 excludes neo-chartalism, market monetarism, and Paul Krugman.

A handful of the Levy Institute’s working papers and policy briefs related to the neo-chartalist approach can be read here: “Money,” “Deficit Hysteria Redux?“, “Money and Taxes,” “Modern Money.”

Comments

Michael Stephens | January 10, 2012

Courtesy of INET, here is Pavlina Tcherneva explaining her “bottom up” approach to fiscal policy.

Notice the way she uses the term “trickle down” to apply also to conventional pump-priming fiscal policy (targeting growth and hoping for the right employment side-effects). We need to move beyond the conventional options on fiscal policy, says Tcherneva; beyond a fiscal policy space marked out by aggregate demand management on one end and austerity on the other. There’s a third approach that’s more in tune with the “original Keynesian spirit,” as she puts it: directly employing the unemployed. We should be targeting employment and the unemployed directly rather than trying to achieve this through the kind of bank-shot maneuver represented by conventional pump priming.

You can read some of Tcherneva’s work on this issue here and here. One-pager here.

Comments

Michael Stephens | January 5, 2012

Via Matías Vernengo, here is the audio of James Galbraith’s keynote address at the ANPEC (Associação Nacional dos Centros de Pós-Graduação em Economia) conference in Brazil. Galbraith addresses the global financial crisis and the intellectual reactions (or non-reactions) to it, dealing both with those who attempted to explain away the crisis and those with a “rage to return” who scrambled for past insights. Here Galbraith has in mind what he regards as the superficial return to Keynes in the early portion of the Great Recession: “Half-remembered insights were framed into half-measures advocated by Keynesians of convenience. … [T]he authority that continues to be associated with Keynes was invoked to deflect and bury his spirit.”

Galbraith also talks about the Marxian, Godleyan, Minskyan, and “Galbraithian” (John Kenneth) schools of thought (which he likens to “Millenarian sects”), joined by their acceptance of the possibility and likelihood of crises, and runs through the differences in their approaches to thinking about financial crises.

Comments

ShareThis

ShareThis