Why Greece Can’t Wait for the Long Run

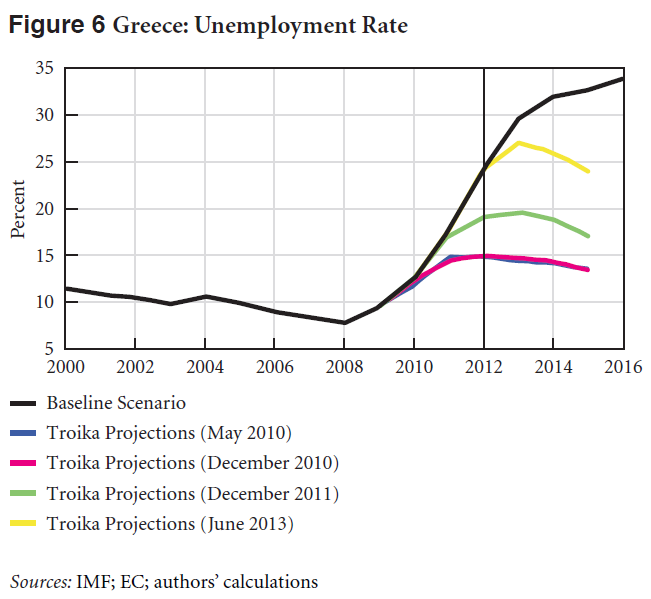

The policies Greece has been implementing as part of the price for its two bailouts are not working the way we were told they would. That’s pretty clear if you look at the troika’s endlessly downgraded projections for key economic indicators. Here, for instance, is actual Greek unemployment, compared to a series of troika projections (source):

One common response to these apparent failures is to say that we just need to hold on, keep the faith, and perhaps double down on the strategy; eventually, internal devaluation and austerity will bear fruit. It is unfortunate, though not surprising, that this has become the “responsible” position; the stance of the supposed steadfast realist.

Presumably it appeals to some deep-seated moral intuitions about the need to pay for past “excesses” or to suffer short-term pain for long-term gain, or some such pablum. And in that context, pointing to increases in poverty, falling living standards, and eye-popping levels of unemployment may not have the rhetorical effect we might hope for, at least among those who see themselves as committed to the policy strategy — perhaps it only reinforces their self-image as defenders of “tough choices” standing steely-eyed in the face of populist clamor.

There are no signs that the internal devaluation strategy is having anything like the effect on growth we were told it would have. But even if we were to grant the assumption that net exports will pick up at some point in the future at a sufficient pace to generate a modest recovery, the problem with the idea that we just need to wait a while longer and cut a little deeper is that we risk serious damage to the tissue of the body politic while we indulge this (we should say radical) intellectual experiment.

The strains are already showing: “While the neo-Nazis won nearly 7 percent of the vote in the 2012 elections, which allowed them to enter parliament with 21 seats, recent public opinion polls suggest that they may now enjoy as much as 20 percent of the public’s support.” This is from C. J. Polychroniou, documenting the recent surge of the neo-Nazi movement in Greece. The policy-prolonged depression isn’t the only reason this is happening, says Polychroniou, noting the history of authoritarian and fascist strains in Greece, but it is playing the key enabling role, he argues: “The surge of neo-Nazism in Greece certainly would not have been possible without the ongoing economic catastrophe and the social decay caused by the policies of fiscal sadism conceived by the EU and the IMF.” (Read the rest here.)

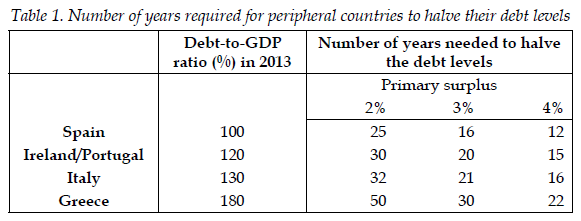

And as for the time horizon of the austerity endgame, take a look at this table from Paul De Grauwe and Yuemei Ji. They’ve calculated how long it would take for countries on the eurozone periphery to halve their debt levels, assuming they run primary surpluses of various sizes (of 2, 3, or 4 percent) and assuming that the nominal interest rate on member-state debt equals nominal growth of GDP (which, as they point out, is not yet the case).

“The issue,” they write, “is whether their political systems will have enough resilience to maintain such ‘temporary’ austerity programmes in order to slowly and painfully draw down the levels of debt.” Even if you’re able to manfully wave away all the waste of human potential that will result from sticking to the policy status quo, betting that Greece’s social and political fabric can hold out for this long is a risky, irresponsible gamble.

ShareThis

ShareThis