The US Senate investigation of JPMorgan Chase’s Chief Investment Office (CIO), and more specifically of the operations of its Synthetic Credit Portfolio (SCP) unit — otherwise known as the “London Whale” trades — concluded with the release of their full report in March. The report alleges that the CIO operated without a clear mandate and that its hedging activities were inappropriate. Neither of these claims, says Jan Kregel, gets to the real problem with the London Whale episode:

The problem arose when JPMorgan Chase created the equivalent of a shadow bank that funded the SCP’s short positions through what was in effect a Ponzi scheme. Further, while proprietary trading was involved in the losses, the real problem was that the bank was allowed to operate across all aspects of finance and the difficulties that this creates for efficient macro hedging. If we are to reduce systemic risk, not only must banks provide regulators with more detailed information on their balance sheet hedging, but it is also necessary to rethink the 1999 Financial Services Modernization Act, as it has led to banks that are too big to fail, manage, or regulate.

Benjamin Lawsky is the very first Superintendent of the New York Department of Financial Services (DFS), a regulatory body created in 2011 through the merger of the New York State Banking and Insurance Departments. Lawsky spoke recently at the Levy Institute’s annual Minsky conference and he began with an appropriately Minskyan tune:

There is a constant danger that putting a thumb in the dyke in one part of the financial system will cause a leak to spring somewhere else. It’s a danger that well-intentioned reforms could push risk to ever-darker corners of the financial system, to financial products not yet envisioned by even the most farsighted regulators. … This is not to say, as some have suggested, that the art of financial regulation is a futile endeavor. … It just means that we should approach the constantly evolving landscape of the financial sector with, in my opinion, a deep sense of humility about the capacity of any one set of reforms or safeguards to permanently preserve the stability of our kinetic, frenetic, global financial system.

Hyman Minsky had definite views about how the financial structure should (and should not) be altered so as to create a more stable and prosperous capitalism, but he also emphasized that the work of financial regulation is never done. It is part of the nature, part of the bargain, as it were, of finance-driven capitalism that new practices and sources of instability are constantly emerging.

In his speech, Lawsky described some concerning new developments in the financial sector, including a below-the-radar practice that garnered the attention of the DFS (ultimately resulting in a series of settlements, one of which was announced about an hour before Lawsky’s speech). continue reading…

When top managers at our largest financial firms claim to have been oblivious of dangerous financial practices carried out under their watch, the most serious implications for regulatory reform don’t actually follow from scenarios in which these managers are lying. It’s a bigger deal, in terms of how far we need to go in changing the way we regulate the banking system, if they’re telling the truth.

Bad apples, after all, can be replaced. But what if the ignorance is real; if managers really don’t know what’s going on in the units below them due to the sheer complexity of the financial institutions they’re running? This might be thought of as a convenient excuse; a universal “get out of jail free” card. But if true, it has more far-reaching, radical implications than most Bankers Behaving Badly scenarios, because it points to a problem that touches on the very structure of the financial system and its key institutions.

This, says Jan Kregel, is part of the the deeper lesson of JP Morgan Chase’s “London whale” fiasco. In a new policy brief, Kregel reviews the recent Senate Permanent Subcommittee on Investigations report on JP Morgan Chase’s difficulties and draws out the lessons for financial reform:

The most probable explanation of the misinformation concerning the “London whale” affair is a massive failure of managerial direction and control that was not the result of deliberate deception, but rather the natural response of individuals who were being paid handsomely to take responsibility but simply did not know what was going on because the size and complexity of the organization made that impossible—again, evidence of an institution that was too big to manage effectively and, a fortiori, too big to regulate.

And as Kregel emphasizes, although it’s not size per se that is problem, but rather the complexity of the institution, there’s often an intimate connection between them: “While complexity is clearly a bigger threat to financial stability than large size, it is usually, but not only, large size that induces complexity.”continue reading…

Jan Kregel speaks at INET’s “Changing of the Guard?” conference in Hong Kong about the tensions between China’s highly regulated financial system and its efforts at rebalancing. Kregel compares elements of China’s financial system to what the United States had under Glass-Steagall and observes that, similar to the US experience, a de facto liberalization is occurring in China through the emergence of shadow banking:

There have been many concerns expressed on the internet about the eventual necessity of reversing the Fed’s cheap-money policies, which include “quantitative easing,” as well as a near-zero federal funds rate.

One idea some have is that there are “too many bonds” in the Fed’s portfolio, and that problems will occur with insufficient demand whenever the Fed attempts to reduce its holdings. This doomsday scenario often seems to vex public discussion but is unlikely to materialize, given that the Fed can always make use of its ability to “make a market” for Treasury securities.

An alternative way of looking at the same situation is that there is a huge amount of money and money-equivalents on bank balance sheets and in nonfinancial corporate coffers, and that the tendency of the modern economy toward financial fragility will eventually lead to risky loans and investments using these funds. (Jeremy Siegel adopts this view in the FT, with, however, an unfortunate emphasis on the possibility of a takeoff of inflation. Inflation remains below the Fed’s 2-percent approximate objective, and the greater risk by far is still recession. An Alphaville comment on his column makes the point that the threat of fragility remains regardless of whether banks have excess reserves on hand.) Concerns have already emerged about “junk” bonds, so-called leveraged loans, and other effervescent areas of finance. Of course, the problem then becomes for the authorities to implement an appropriate restraint on financial excesses. One conventional method would be to increase interest rates using open-market operations, which would of course probably entail the sale of securities. This scenario unfortunately might lead to some serious threats to financial stability, including problems that short-term and/or variable-rate borrowers might have meeting payment commitments on their debts, if the Fed were to raise interest rates sharply.

One big historical example of this kind of fragility is the rise in short-term interest rates that occurred in the late 1970s and early 1980s at the behest of the Fed. The resulting delta-R effect helped to bankrupt Mexico, among other disastrous impacts. Many years before that, the Fed was more inclined to use direct controls on credit, restricting the amount of money banks could lend out.

Key to the situation today, efforts are ongoing in Washington to formulate and implement appropriate rules to insure that various kinds of bank lending do not get out of hand in the first place. Efforts of this type would be unlikely to completely prevent future crises, but, if effective, would act to reduce fragility. Among other benefits, this approach might also permit the recovery in housing investment—currently only in a fledgling phase—to continue. Given the problems that sharp interest-rate increases can bring, it would also be helpful to keep the effects of moderate inflation in perspective, and to cope with inflation in non-destabilizing ways.

In a new, wide-ranging policy note, C. J. Polychroniou traces the roots and evolution of the present “era of global neoliberalism”; an era he portrays as mired in perpetual crisis and dysfunction, and ripe for change.

[N]eoliberalism itself is more of an ideological construct than a solidly grounded theoretical approach or an empirically-derived methodology. In fact, the intellectual foundations of neoliberal discourse are couched in profusely vague claims and ahistorical terms. Notions such as “free markets,” “economic efficiency,” and “perfect competition” are so devoid of any empirical reference that they belong to a discourse on metaphysics, not economics.

Polychroniou attempts to outline the central principles of a progressive, post-Keynesian economic policy alternative. His primary target: changing the relationship between the state and the financial sector.

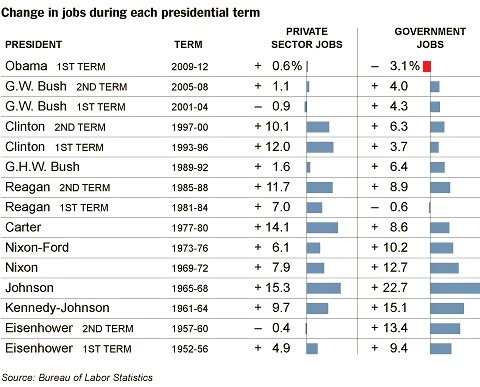

Randall Wray joined Suzi Weissman on her “Beneath the Surface” radio show on Friday. They began the interview with a discussion of the policy blunders that are creating headwinds for the US economy, including the expiration of the payroll tax cut, the decline of real per capita government spending, and, as Wray put it, “the government sucking jobs right out of the economy.” He’s not referring here to the walking corpse of the theory that regulatory uncertainty is to blame for the slow recovery, but to the fact that government is holding back job growth far more directly: by laying off workers at an unprecedented rate. For context, look at this chart put together by Floyd Norris (highlighted):

They also addressed thisMarketplace segment on the “death of inflation,” ongoing threats from the financial system, and some ideas for financial reform that are currently being tossed around. On the latter, Wray argued that the idea of a financial transactions tax (being considered by a number of EU countries) is a second-best or partial solution. Instead of sin taxes and other such “economists’ solutions,” as he described them, Wray recommended coming at the problem more directly: by outlawing certain speculative activities and going after practices like high-frequency trading. They closed with a discussion of the prospects of another financial crisis emerging.

Salim B. “Sandy” Lewis in conversation with Matt Taibbi

Tuesday, February 19, 7 pm

Bard College, Annandale-on-Hudson, NY

Room 103, Reem-Kayden Science Building

Lewis will explore “Why Fixing Wall Street and the Economy Is Critical to the World” in a discussion with Matt Taibbi, the renowned political and financial columnist for Rolling Stone. The discussion will be moderated by Roger Berkowitz, academic director of the Hannah Arendt Center for Politics and Humanities at Bard. Following the talk, Lewis will take questions.

Some of Lewis’s criticisms of Wall Street appeared in an Op-Ed essay in the New York Times. He has been featured as well in a Times profile in 2012.

In the latest phase of our endless budget brinksmanship, congressional Republicans will attempt to extract policy concessions in return for raising the debt limit (Republicans are not only demanding cuts to Social Security and Medicare—they are brazenly demanding that Democrats propose, and therefore own, these unpopular cuts). The administration and key allies are claiming they will not negotiate over the debt limit.

At stake in this standoff is not just whether the federal government will default on its financial commitments (which is to say, whether Congress will absurdly prevent the government from paying the bills that Congress has legally obligated it to rack up) but also whether we will move one step further toward making these standoffs a customary part of the (mal)functioning of government.

In the context of some key changes made by the Dodd-Frank Act, this new normal on the debt ceiling has disquieting implications for how the federal government will respond when the next financial crisis hits. Dodd-Frank doesn’t do much to prevent the next crisis from emerging, but it does change the way the government can respond. At last year’s Minsky conference in New York (see Session 6), Morgan Ricks noted that a number of organizations that played a large role in the response to the financial meltdown (Fed, Treasury, FDIC) have seen their discretionary authority limited by Dodd-Frank. Most notably, the Federal Reserve’s leeway under section 13(3) of the Federal Reserve Act has been curbed (13[3] allowed the Fed to lend, “under unusual and exigent circumstances,” to individuals, partnerships, and corporations at its own discretion; it was under this authority that most of the unconventional lending and asset purchases were carried out).

After Dodd-Frank, Ricks observed, we are now supposed to rely on the FDIC’s newly-created “Orderly Liquidation Authority” (OLA) to handle the collapse of a large multifunction financial institution. The use of the OLA requires the approval of the Treasury Secretary and two-thirds of the both the Federal Reserve board and the FDIC board, but most importantly, funding for the OLA will come from the Treasury rather than the Federal Reserve. Ricks pointed out that since the Treasury would have to issue debt to provide such funding (assuming platinum coins are off the table), this means that a future government rescue through the OLA may require that Congress lift the debt ceiling in the midst of a financial emergency. You might say this adds a laudable element of accountability and transparency to any future crisis response. But after watching Congress perform these past two years, how confident are you that this will end well?

From 2009 to 2012, the US federal deficit shrank from 10.1% of GDP to 7% of GDP. That’s the fastest deficit reduction we’ve seen in six decades—and all before the fiscal cliff has kicked in. Here’s the chart from Jed Graham:

Put this alongside a record-setting contraction of government employment and a 7.9 percent unemployment rate, and what you have is a portrait of fiscal irresponsibility. A lot of this deficit reduction has to do with the fact that the economy is now growing (albeit feebly), instead of contracting, but looking at this chart should also reinforce how dangerous and unnecessary it is that we’ve decided to create an austerity crisis at this moment. (This “austerity crisis,” by the way, should really be understood to include both the possibility of going over, and staying over, the fiscal cliff AND the possibility of the cliff being replaced by a “grand bargain” on deficit reduction.) The last time the deficit was reduced at a faster rate was in 1937, when the government embraced a hard pivot to austerity and the economy tumbled back into recession.

But don’t worry, we aren’t reliving the history of the 1930s. Not exactly. We are combining fiscal irresponsibility with regulatory negligence. The Financial Stability Board (FSB) reported on Sunday that the shadow banking sector, after contracting in 2008, has rebounded nicely and is doing just fine. Although it hasn’t quite seen the growth it did prior to the crisis, when it doubled in size from 2002 to 2007 (from $26 trillion to $62 trillion), the shadow banking sector reached $67 trillion globally in 2011—a new record, and “equivalent,” says the FSB, “to 111% of the aggregated GDP of all jurisdictions.”

ShareThis

ShareThis