Save the Date: 12th International Post-Keynesian Conference

I recently had the great fortune to listen to a speech delivered by Mr Yves Mersch, Member of the Executive Board of the European Central Bank. This was in Athens on November 8 at the first Minsky Conference in Greece organized by the Levy Economics Institute. The title of the conference was “The Eurozone crisis, Greece, and the Austerity Experience.” The conference was well attended by the interested public. As is typical of Minsky conferences, annually held in the United States, it brought together academic scholars, financial market practitioners, journalists, as well as policymakers, including Mr. Mersch, whose speech was titled “Intergenerational justice in times of sovereign debt crises” (see here). Mr Mersch played part in the negotiations of the Maastricht Treaty and has served as the Governor of the Central Bank of Luxembourg since its formation in 1998, before joining the ECB’s Executive Board last year.

Apart from lauding Greece’s pension reforms as measures that were necessary in view of demographic trends, Mr Mersch hailed Greece’s achievements in closing its fiscal deficit as “remarkable,” describing the Greek austerity experience as a “fiscal adjustment of historic proportions.” That it truly was, and Mr Mersch was keen to emphasize that the “extraordinary efforts” undertaken by the Greek people refuted the naysayers and proved wrong prophetic claims heard in May 2010 that Greece would leave the euro area within months. Mr Mersch acknowledged that record-high unemployment was a “tragedy,” only to go on to assert that “this is the painful cost of reversing the misguided economic policies and lack of reforms in the past.”

And, of course, more of the same would be needed, according to Mr Mersch: more fiscal consolidation, more structural reforms, and lower wages and prices in order to increase external competitiveness and facilitate an export-led recovery, as Greece’s “external sector must go into surplus.” This may be painful, “but we are in a monetary union and this is how adjustment works.” In addition to more wage-price deflation, Mr Mersch singled out the need to restore the health of Greek banks and the need for attracting more foreign investment as the other key ingredients that would deliver adjustment and recovery in Greece.

During the Q&A session following his speech I asked Mr Mersch whether there might not be a conflict between, on the one hand, emphasizing the need of healthy banks that would fund the recovery and, on the other hand, prescribing more wage-price deflation. Since a deflationary environment was not exactly known as a factor that would tend to improve the health of banks. And I also asked him why the ECB was tolerating such a significant undershooting of its 2 percent stability norm while calling for even more wage-price deflation in crisis countries – instead of going for higher inflation in current account surplus countries such as Germany. At least to me it seemed obvious that a properly stability-oriented central bank should much prefer inflation in surplus countries to be sufficiently high so as to enable the bank to actually meet its mandate, that is, 2 percent HICP inflation on average across the currency union, over an outcome where even Germany has an inflation rate that is well below 2 percent, with the ECB ending up sharply missing its self-defined target in the downward direction.

Mindless austerity or stability-oriented austerity?

Mr Mersch’s answers were very interesting. continue reading…

Is the U.S. economy heading towards another bubble? Since last week, the number of commentators on this subject has been growing, from Robert Shiller to Nouriel Roubini (on housing markets).

In our first chart we report the Standard & Poor’s 500 stock market index, normalized by a consumer price index to remove the common trend in prices. Our measure has increased by 105.6 percent from its most recent bottom in March 2009. In the previous rally, which started from a bottom value in February 2003, the index increased by only 63 percent before the start of a rapid descent in July 2007.

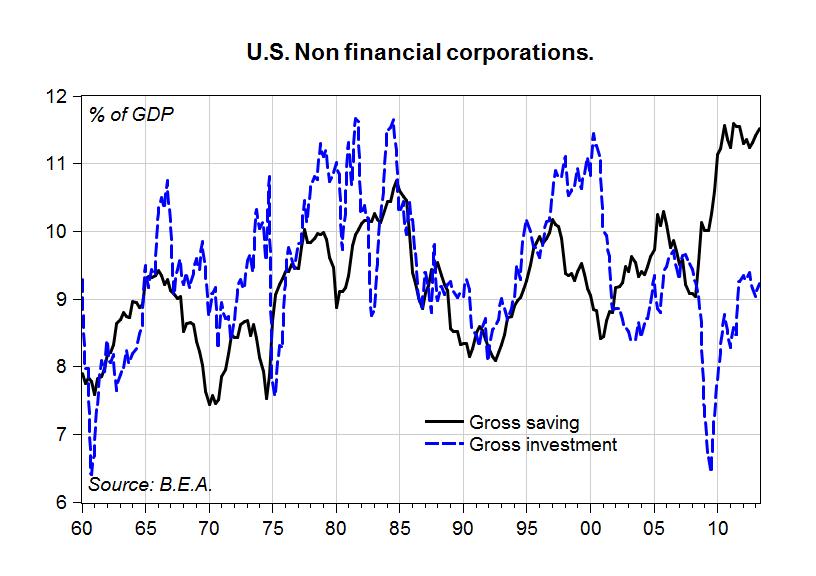

Is a buoyant stock market justified by expected profitability? In the next chart, we report gross saving of non-financial corporations – that is, undistributed profits gross of capital consumption – scaled by GDP, along with gross investment (which includes changes in inventories). All figures are computed from the Integrated Macroeconomic Accounts published by the B.E.A.

The chart clearly shows that profits have reached an all-time high at 11.5 percent of GDP, compared to an average of 9 percent over the 1960-2007 period. If current profits are the basis for expected future profitability, our data suggest that the stock market rally is justified. But is this trend stable and sustainable?

The chart also shows what we may call an investment gap. While profits and investment have usually moved in line, it was usually the case that investment exceeded retained profits. But since the second half of 2008, profits have soared while investment dropped, opening a gap which is currently over 2 percent of GDP. A low level of investment is not a good sign for future growth.

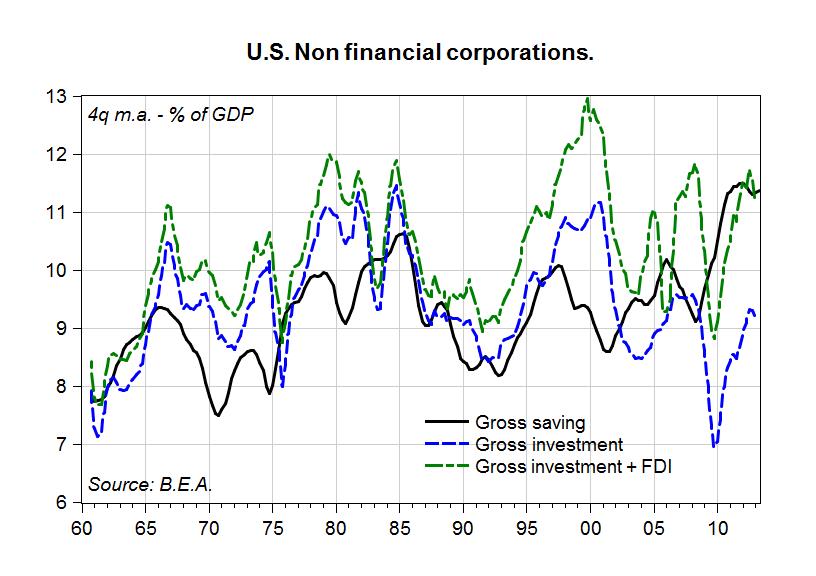

What are companies doing with such exceptional profits? In the next chart we add U.S. foreign direct investment (FDI) made abroad to domestic investment in our previous chart (while at the same time switching to moving averages to reduce the volatility of quarterly FDI).

The new chart is suggesting that foreign direct investment is a major destination for retained profits, and that FDI did not suffer the same downturn seen in domestic investment during the last recession.

Data from the B.E.A. on the composition and direction of U.S. FDI show it is difficult to evaluate where U.S. foreign direct investment is directed. While data for FDI in manufacturing show the emerging role of China as recipient of U.S. FDI, its weight is still below 5 percent of total FDI in manufacturing. Besides, the share of manufacturing in total FDI in 2012 is only 14 percent, while multinational companies, classified as “Holding Companies (non bank)” in B.E.A. statistics, account for almost 44 percent of total FDI in 2012. Countries receiving FDI in this grouping seem to be financial centers: the Netherlands (25.6 percent), Luxembourg (15.5 percent), Bermuda (11.2 percent), and the U.K. (10.7 percent).

Summing up, our findings suggest that U.S. non-financial corporations are in a healthy state – as measured by their net profits – but that this will not necessarily imply stronger U.S. growth and job creation. On the contrary, the data are coherent with a further increase in the concentration of income leading to financial speculation, in the U.S. as well as in foreign financial markets.

Restoring jobs and prosperity in the U.S. does not seem to be what U.S. corporations are working towards, and yes, the soaring stock market may change course very quickly, if “financial markets” make this decision.

Restoring sustainable growth in the U.S. (and elsewhere) requires a reversal of the trend in income distribution, since, as Stockhammer reminds us, “rising inequality has increased the propensity to speculate as richer households tend to hold riskier financial assets than other groups,” and “higher inequality has led to higher household debt as working class families have tried to keep up with social consumption norms despite stagnating or falling real wages” – a fact we already investigated a few years ago.

ShareThis

ShareThis