This Time Is Indifferent

Whether it’s the terrible growth numbers in the eurozone (Eurostat), the revelation of spreadsheet errors in everyone’s favorite debt disaster study (for some of the non-spreadsheet-based problems with the Reinhart-Rogoff approach, see this 2010 working paper), or the fact that the US federal deficit is on track to shrink to a measly 2.1 percent of GDP in two years (CBO report here), the past couple months have offered up some embarrassing and inconvenient news for those who continue to push for austerity.

Nonetheless, we’re unlikely to see any of this dramatically alter the budget debate, and the key to understanding why is to appreciate that there is a significant constituency among austerity supporters for whom most of this data is irrelevant. It’s not just that this information isn’t likely to persuade them, but that for a certain species of austerian, it couldn’t possibly. After four years of fiscal fear-mongering, it has become clear that for some ostensible austerity supporters, it was never really about the deficit.

With last week’s updates, the CBO now predicts that the budget deficit will fall to 2.1 percent of GDP by 2015. If that number means nothing to you, consider that the original Bowles-Simpson plan — the standard by which budget seriousness is measured in the press — called for a 2015 deficit of … 2.3 percent of GDP. Pikers.

Yet, revealingly, there are some deficit hawks who are treating the rapid shrinking of the deficit as bad news — and not for the Keynesian reason that this indicates the government is failing to do its part in supporting the economy, as Bernanke stressed in his remarks yesterday, but because the disappearing deficit is easing congressional pressure to pass “entitlement reform” (which, as we’ll see below, does belong in scare quotes).

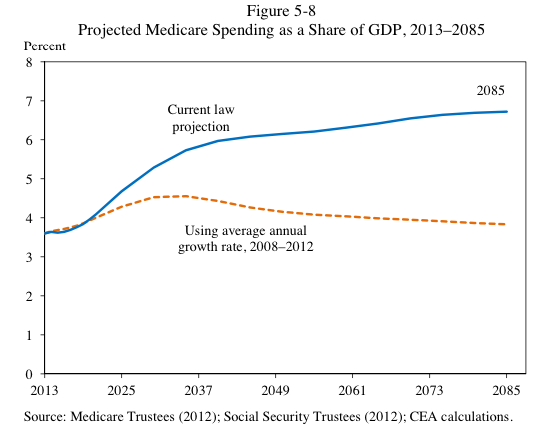

And lest you think this is all about concern for the long-term deficit, note that one of the reasons projections of future deficits have been falling is due to a slowdown in the growth of healthcare costs. If this slower rate of cost growth maintains itself for any significant period of time, the story we’ve been hearing with regard to the long-term budget changes dramatically. Here, according to the CEA‘s Economic Report of the President, is what Medicare spending will look like over the long term if the more recent trend in healthcare costs sticks:

Although it’s roundly denied, entitlement reform has already passed, and there is some initial evidence to suggest that the cost control measures in the Affordable Care Act might be playing a role in the slowdown in healthcare spending. Yes, there are a lot of “ifs” here, but it’s curious that purported deficit hawks seem so disinterested in these developments. Real entitlement reform apparently means raising the eligibility age for Medicare. But notice that this proposal would end up increasing healthcare costs for individuals, businesses, and states by twice as much as would be saved by the federal government, and the budget savings themselves would be relatively small, at around $5.7 billion in 2014. Whatever leads you to imbue this proposal with such significance while sniffily dismissing the ACA — presumably part of the appeal of the former is that it reduces the role of public insurance — it’s hard to see that it has much to do with concerns about deficits and debt per se.

If you want to look on the bright side of all this bad faith, it suggests that there may be fewer people who were genuinely swayed by the macroeconomic arguments in favor of austerity. For the fauxsterian, the question of whether austerity can be expansionary, or whether economic growth falls off a cliff when countries’ public debt ratios surpass 90 percent of GDP, is really all beside the point. Deficit and debt hysteria have simply been a useful tool for pushing specific legislative changes that may or may or may not be related to the budget balance — changes that might be difficult to pass outside an atmosphere of imminent crisis.

A recent Washington Post column by Steven Pearlstein, “The Case for Austerity Isn’t Dead Yet,” more or less endorses this line. The problem with fiscal stimulus, the column tells us, is that it works: it boosts short-term economic growth, thus easing the pressure to pass “structural reform.”

It would be preferable if we could move this argument to the foreground. Is increasing the probability of passing structural reform so valuable that it’s worth, for instance, maintaining depression-level unemployment rates in Greece? Presumably that depends on the relative probabilities and what we mean by “structural reform.” Pearlstein tells us that it includes “regulations” and “privatizations.” So is it worth it to tolerate 27 percent unemployment if this gives us a better chance at privatizing more Greek public assets? It’s hard for me to see how you could make that argument without wildly overestimating the benefits of (further) privatization and/or significantly discounting the interests of the average Greek citizen. But by all means, let’s have that argument, and dispense with the pretense.

ShareThis

ShareThis

Economic growth falls off a cliff when countries’ household debt ratios surpass 90 percent of GDP.