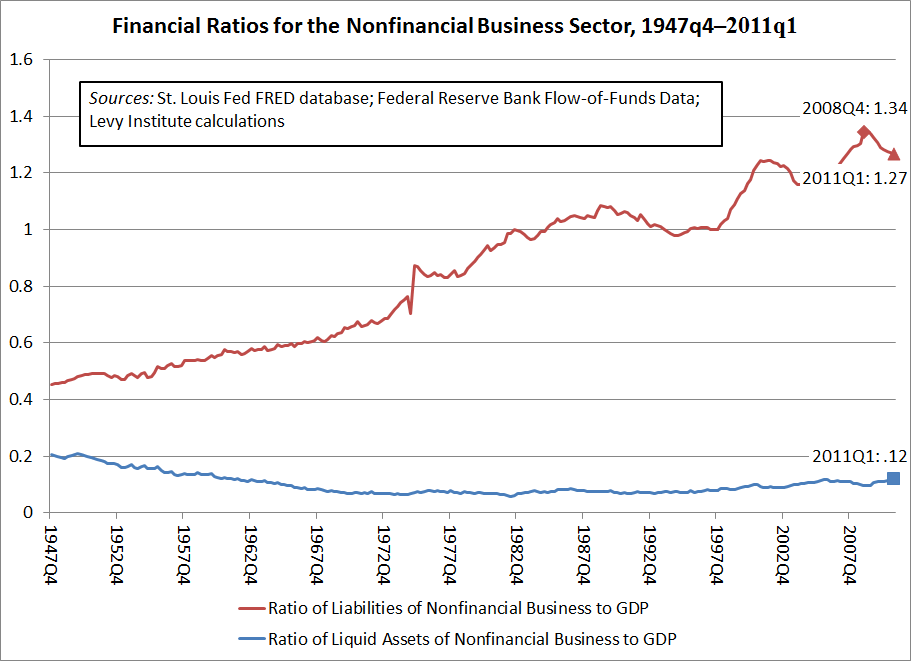

Private-sector debt ratios still high by historical standards

With all the recent coverage of the federal government’s debt-limit impasse, it has been some time since the private sector’s financial picture has received much attention in the popular press. Nonetheless, there seems to be little news, as the most recent flow-of-funds data release from the Fed depicts a continuation of trends that have held for at least the past two years or so. Specifically, for the business sector, the figure below shows declining ratios of debt to GDP and increasing ratios of cash-like assets to GDP. (You may need to click on the image to make it large enough.)

(Liquid assets include checking and savings accounts at banks, Treasury securities, and currency, all of which can be useful in avoiding missed payments, etc., when financial stresses arise. Also, assets and debts are of course measured in terms of dollars, rather than numbers of bonds, shares, etc. In all of the financial ratios discussed in this post, GDP is expressed in terms of seasonally adjusted output per year, though the data are for individual quarters.)

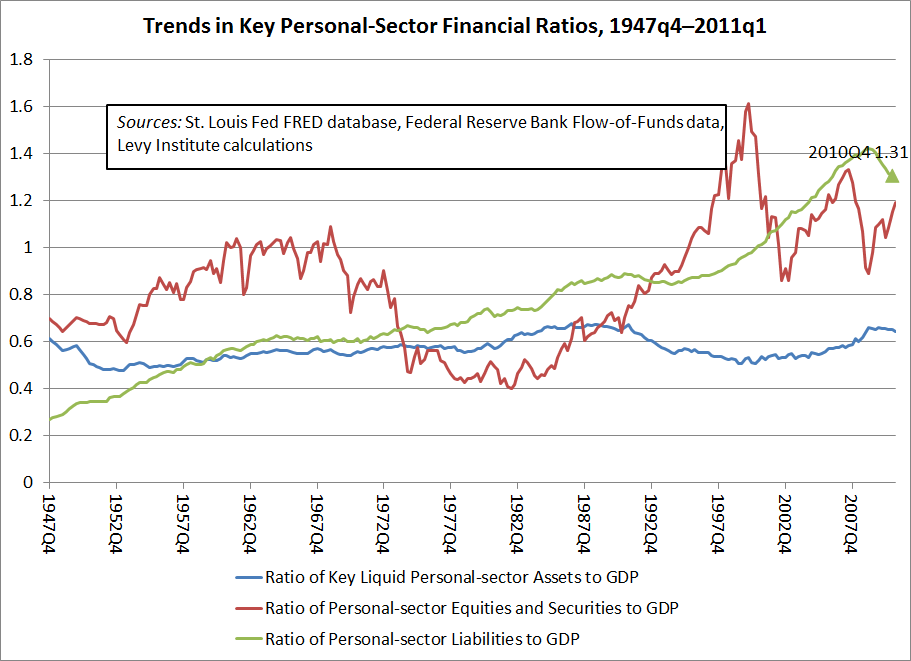

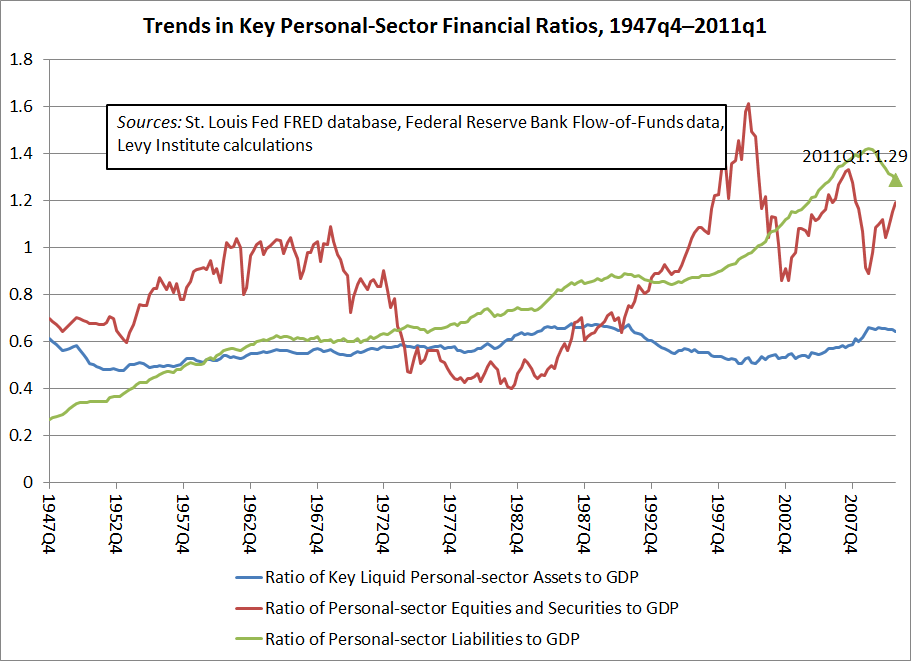

In the next figure, shown below, we can see that the personal sector (households, small businesses, and nonprofit organizations) has experienced increasing ratios of securities holdings to GDP in recent quarters, along with falling ratios of liquid assets to GDP. Moreover, as a percentage of GDP, the liabilities of this sector, too, have been falling.

The falling private-sector debt-to-GDP ratios are not surprising in light of the recent financial crisis and the collapse of the real estate market, which not surprisingly led to a retrenchment in many forms of lending, as well as many defaults. Some will find it remarkable that private-sector debt has fallen so rapidly, but for a number of reasons, financial crises are typically followed by at least a partial turn toward financial conservatism and reregulation. Also, the weak economy has naturally curtailed the kinds of spending that are often fueled by new borrowing. On the other hand, the nearly relentless upward trends shown throughout both figures put more recent declines in private-sector debt into perspective. These long-run trends reflect what can be thought of loosely as a gradual increase in U.S. financial fragility beginning in the aftermath of World War II, in the 1940s. Levy Institute scholar Hyman Minsky was noted for observing this trend and warning of the threat it posed.

Update, July 27, 2011: I have made a few changes to this post to improve its clarity. Also, to see all comments on this post, please click on the link below. -G.H.

ShareThis

ShareThis{kind=link}

[…] update (July 27, 2011): Multiplier Effect, the blog for the Levy Economics Institute, has more data. […]

“Some will find it remarkable that private-sector debt has fallen so rapidly”

Not really. It’s been piled onto the public accounts.