Euroland’s “Recovery” – Three Cheers for Dr Schäuble!

(first appeared in Social Europe)

Never miss a party – especially one you’ve been desperately waiting for for so long. This much the authorities in Europe’s currency union clearly understand. As soon as Eurostat had released its first estimate for GDP growth in the spring quarter in mid August (1st estimate here), which was missing the by now customary negative sign, the champagne began to flow, it seems, accompanying all-round self-congratulatory shoulder slapping.

For instance, Spain’s economy minister Luis de Guindos confidently noted that “Spain will show clearly the quality of the policies implemented in the eurozone” (FT.com 4 September 2013). And European Commission President José Manuel Barroso declared in his State of the Union Address on 11 September 2013 that “the facts tell us that our efforts have started to convince.” Germany’s finance minister Wolfgang Schäuble also joined the chorus, just in time for the federal election, proudly announcing in The Financial Times that “while the crisis continues to reverberate, the eurozone is clearly on the mend both structurally and cyclically.” Dr Schäuble declared with poise that “what is happening turns out to be pretty much what the proponents of Europe’s cool-headed crisis management predicted. The fiscal and structural repair work is paying off, laying the foundations for sustainable growth,” and then went on to boast that “despite what the critics of the European crisis management would have us believe, we live in the real world, not in a parallel universe where well-established economic principles no longer apply” (“Ignore the doomsayers: Europe is being fixed,” FT.com 16 September 2013; see comment by this author: “The euro crisis is not even close to being over, Mr Schäuble”).

Apparently Germany’s “stability-oriented” prescriptions for the land of the euro are now doing their magic just as Dr Schäuble had always promised they would. Fiscal contractions are now proving expansionary after all, just with a little bit of a delay, while growth-enhancing structural reforms are beginning to bear fruit too, it seems. The euro authorities are making sure though not to miss any chance at emphasizing that more of the same medicine will be needed to do even more good going forward.

Perhaps this is a good time then for a reality check. Eurostat estimates that Euroland’s GDP has grown by 0.3 percent since the winter quarter (2nd estimate here). The first thing to note is that the news refers to quarter-on-quarter growth as Euroland’s economy is still half-a-percent smaller than it was a year ago. The next thing to note is that the focus on GDP growth is grossly understating the true damage caused by “cool-headed crisis management” in the past few years. Much in contrast to other regions of the world, Euroland’s recovery from the global crisis was cut short in 2011 when the area prematurely embarked on mindless fiscal austerity.

Of course the damage was concentrated in euro crisis countries that, owing to euro design flaws, found they had no choice but to comply with the kind of policies Germany called for. The point is that Germany too, and without facing any such market pressures, actually quite the opposite, joined the fiscal austerity crusade, as Dr Schäuble firmly believes that balancing the public budget and paying off the public debt are the primary goals of fiscal policy anyway. To foster this end, and also to counter pressures that call on Germany to actually contribute toward rebalancing Euroland, Germany appears to systematically understate its fiscal position.

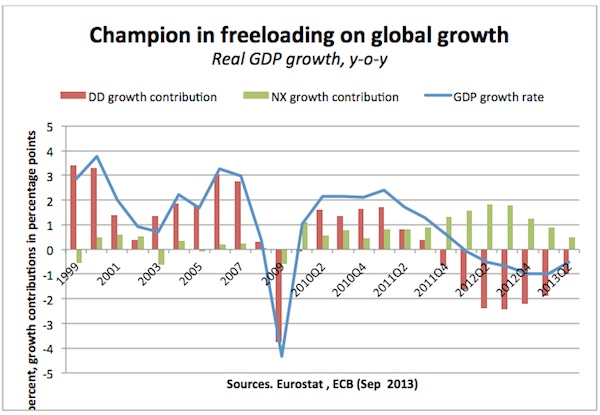

Be that as it may, Euroland entered recession in the final quarter of 2011, a recession that was to last six quarters. Last summer domestic demand was falling at an annual rate of over 2 percent. To be sure, this was by no means as rapid a rate of decline as seen in the freefall episode in 2008-9, but the shrinkage lasted unusually long, owing to amplification by persistently procyclical fiscal policies. Luckily, throughout the protracted decline in domestic demand, Euroland could hold on to an external lifeline courteously extended by the rest of the world: positive growth contributions from net exports offset about half of the damage done by Messrs Schäuble and Co. at the home front.

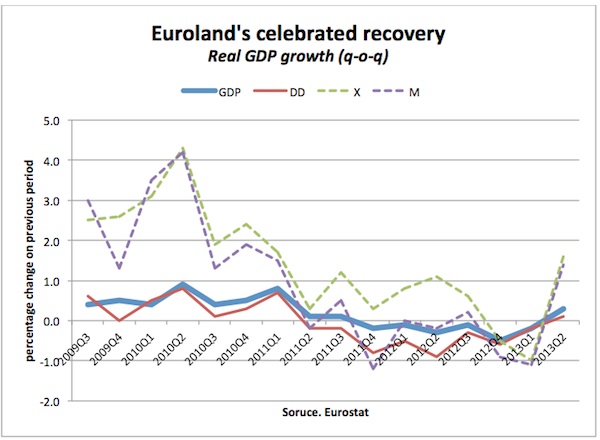

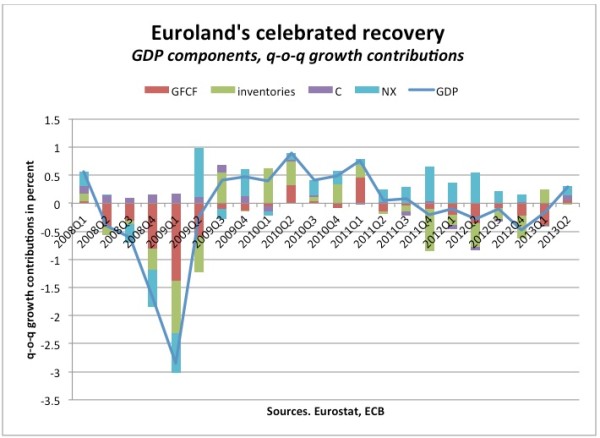

Turning now to quarter-on-quarter growth numbers, we see that the rebound in the second quarter owed both to a rebound in global trade, following a two-quarter decline in Euroland’s exports, and a stabilization of domestic demand, following eight – yes, eight! – consecutive quarters of decline. Essentially, fixed capital formation finally stabilized while consumption eked out a little bit of a rise. In terms of growth contributions, the spring “recovery” owes two-thirds to next exports and one third to domestic demand. That said, given that domestic demand still subtracted from GDP in the winter, this truly is a bit of good news.

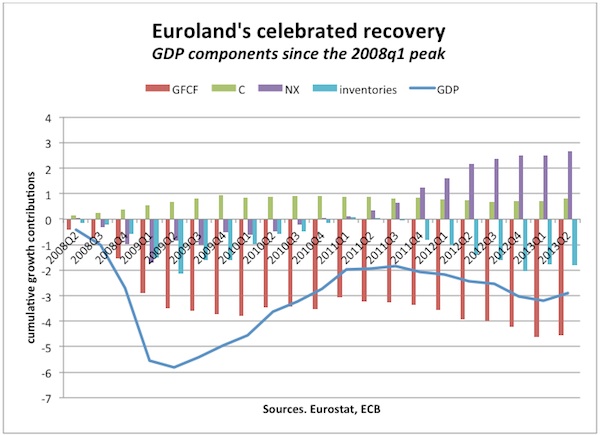

However, to put things into perspective, one might also want to take a look at growth contributions of GDP components since the peak in Euroland’s GDP in the first quarter of 2008 (approximated here by cumulating q-o-q contributions). To begin with, as to overall GDP, Euroland suffered 6 percent of shrinkage in the global crisis, two-thirds of which it had temporarily recovered by 2011, when it fell back into its purely homemade recession. Today, the Euroland economy is still 3 percent smaller than in the first quarter of 2008. The dismal situation owes itself mostly to severely depressed fixed capital formation. Fixed investment plunged in 2008 and has seen no meaningful recovery since. But at least it is no longer shrinking today.

That alone appears to have sparkled some fantasies and has the euro authorities rolling out the champagne, it seems. Quite a party will be needed to make up for the lost ground though. And the euro authorities may have to do a disproportionate share of the partying, as neither Euroland’s unemployed – standing at a record high of over 12 percent and still rising – nor those who still have a job but fear losing it, are very likely to join in. Remarkably, wages in Euroland are rising at an even lower rate than Euroland’s extraordinarily low consumer price inflation. Even in Germany, which is at the center of the ongoing “recovery,” employees are barely enjoying any real wage increase. Not to mention the rest. At least the ECB does not appear to be too concerned though, as wages and prices are not falling in Euroland as a whole. Let deflation scares inspire the authorities in the rest of the world to stimulate their economies, and Euroland’s exports along with it, the ECB appears to calculate, following Bundesbank “stability-oriented” wisdom.

But can we really hope that global growth is about to take off again, pulling Euroland along? Too bad the WTO has actually just reduced its forecast for global trade in 2013-4 (see here). Alternatively, will entrepreneurs finally shake off the uncertainties and troubles plaguing Europe’s ill-constructed currency union? Better not bet on that one either, as financial market exuberance has yet to inspire entrepreneurial animal spirits. In Europe’s severely depressed economy, grim sales prospects tightly limit any entrepreneurial joys from squeezing employees ever further. European-style structural reform fosters deflationary tendencies rather than growth. Most likely, the rise in PMIs since the spring is merely reflecting some ongoing “restocking,” which might perhaps give us a couple of quarters of breathing space.

The trouble is that with growth (both real and nominal) as meager as it is, budgetary targets will be missed, hence fiscal drag will continue, and unemployment will stay high or rise even further. And this is assuming that nothing really bad will come in the way (since Mr. Draghi’s magic words are keeping the markets happy forever, if they do). Let’s all celebrate with Dr. Schäuble before it’s too late.

ShareThis

ShareThis