A Continuation of the Fed’s “Cheap Money Policy”?

As I write, markets are wondering what Fed Chairman Ben Bernanke will say about interest rates in a press conference taking place this afternoon. Many economists, including some on the Federal Reserve’s rate-setting committee, are arguing that the Chairman is courting inflation with his policies of keeping interest rates low. He has been using three main approaches to this task:

(1) keeping short-term interest rates low through open market operations;

(2) buying and holding medium- and long-term bonds in a direct bid to keep longer-term rates low; and

(3) saying that it is likely to keep the federal funds rate near zero for an extended period of time.

Task (1) has been the usual approach of the Fed in modern times (since the early 1950s perhaps); task (2) has been important since the Fed’s response to the financial crisis beginning in 2008 or so. The current version of task (2) consists largely of a “twist” operation in which short-term securities are sold to pay for purchases of long-term securities. Task (3) is a commitment of sorts about short-term rates that helps to keep longer-term rates down. Tasks (2) and (3) are the most directly relevant to mortgage and auto loan rates, which are longer-term rates.

Economists, including critics of the Fed’s expansionary policies, sometimes refer to this three-pronged approach as a “cheap money policy,” but many who oppose “cheap money” have claimed that it would not be possible to maintain such a policy for very long (economic laws, or perhaps the bond markets’ worries about future inflation, would prevent this).

In a 1952 essay, Joan Robinson argued that a modern central bank could achieve a low long-term interest rate, but that it would take a long time to do so, in comparison to the quasi-real-time control the Fed enjoys over the federal funds rate. The reason is that the prices of long-term bonds (even risk-free Treasury bonds) depend on expectations about the future prices of these bonds and other securities. Changing those expectations would not be an easy or quick matter.

We have very little knowledge of the influences shaping expectations. Past experience is no doubt the major element in expectations, but experience, as far as one can judge, is compounded in the market with a variety of theories and superstitions and the whole amalgam is played upon day to day by the influences (including the bank chairman’s last speech) which make up what Keynes called “the state of the news”. Any theory that is widely believed tends to verify itself so that there is a large element of ‘thinking makes it so’ in the determination of interest rates. (Robinson, 1952, in “The Rate of Interest” from The Generalisation of the General Theory and Other Essays.)

Hence, there was an inertia in expectations that would make the cheap money policy something more than a matter of mechanically turning a knob for the central bank. Market psychology is also important. In another section of the same essay, Robinson outlines a scenario in which a central bank like the Bank of England could carry out such a campaign to convince bond markets that yields would stay low in the future, protecting the market value of existing bonds. This section has the heading, “A Cheap Money Policy.”

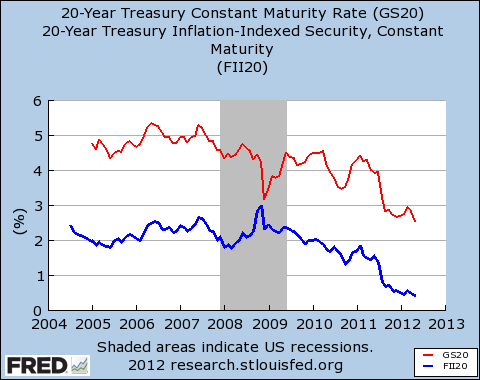

It has been noted by many Keynesians in the blogosphere and elsewhere that nominal and real long-term rates have trended downward since the financial crisis, despite warnings from misguided commentators that high deficits would eventually cause them to rise. Interestingly, rates have fallen rather slowly, in keeping with Robinson’s scenario of gradually easing investors’ fears that bond prices would fall in the future. At the top of this post, we provide an updated figure showing the path of 20-year Treasury bond yields, “real” (blue line) and nominal (red line). The former series reflects the extent of investors’ fears of inflation, i.e. what they are willing to pay for an inflation-indexed return on their investments. Both series reflect their views of future nominal yields.

Note: The official Fed policy statement issued today is available at this link.

ShareThis

ShareThis

[…] year. Keynes’s statement, much like the quote from Robinson mentioned above and the one in this earlier post, foretells this […]

[…] my last post, I quoted Joan Robinson, the renowned Cambridge University economist, on the determinants of […]